As we move through 2025, the industrial real estate sector faces a complex landscape shaped by economic uncertainty and shifting trade policies.

The recent Cushman & Wakefield “Midpoint 2025 Economic and CRE Outlook” highlights a slowdown in industrial demand, driven by tariff-related disruptions and a cooling economy.

Yet, long-term fundamentals remain robust, with supply constraints and manufacturing growth offering hope for a rebound.

In this two-part newsletter, we’ll explore how these dynamics affect industrial real estate, offering insights for investors and occupiers.

For today’s issue, we’ll dive into the current state of demand, vacancy trends, and the impact of global trade on industrial leasing.

Although the report is centered around the American economic landscape, historically, these trends have largely followed north of the border. Whether or not that continues, this data can provide another perspective for where the Toronto industrial market may be headed in the coming months and years.

So without further ado, let’s kick off this series on industrial market dynamics amid economic shifts.

Section 1: Slowing Demand and Rising Vacancy

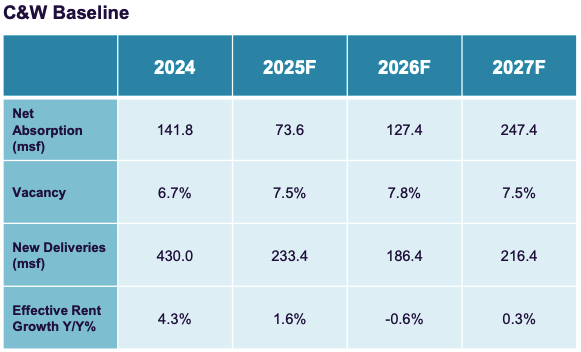

The industrial sector, once a powerhouse of growth, is experiencing a cyclical slowdown. According to Cushman & Wakefield, net absorption in 2024 was 141.8 million square feet (msf), a sharp decline from the 2021 peak, and is projected to drop further to 73.6 msf in 2025.

This trend reflects cautious occupier behavior amid economic uncertainty, particularly due to trade policy shifts. The report notes that demand in 2024 was one-fifth of 2021 levels, and this softness is expected to persist into 2025, with a rebound not anticipated until 2026, when net absorption is forecasted to reach 127.4 msf.

U.S. Industrial Market – Source: Cushman & Wakefield Research.

Vacancy rates are trending higher, rising from 6.7% in 2024 to a projected 7.5% in 2025, where they are expected to stabilize through 2027. This increase is partly due to the record construction boom of recent years, which delivered 430.0 msf in 2024. However, new deliveries are slowing, with 233.4 msf expected in 2025 and 186.4 msf in 2026. High construction and labor costs are limiting new projects, setting the stage for tighter supply and stronger occupancy gains by 2026-27. For investors, this suggests a window to acquire assets in markets with constrained pipelines, where future vacancy compression could drive value.

Rent growth is also softening, with effective rent growth projected at 1.6% in 2025, down from 4.3% in 2024, and dipping to -0.6% in 2026 before recovering to 0.3% in 2027. Markets with demand-led vacancy increases are seeing the most significant rent declines, but the long-term outlook remains positive, with rent growth expected to approach 3.5% by the decade’s end. Occupiers should leverage this period of softer rents to secure favourable lease terms, while investors may find opportunities in high-quality assets poised for future rent appreciation.

Section 2: Global Trade and Tariff Impacts

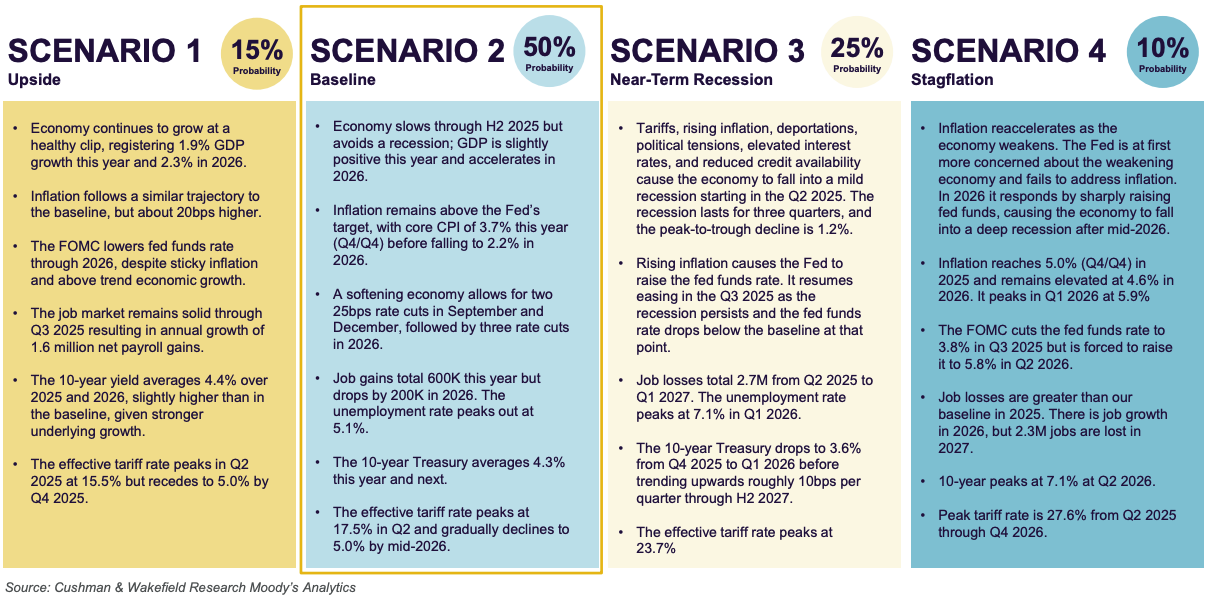

Global trade disruptions, particularly elevated tariffs, pose significant risks to industrial demand. The Cushman & Wakefield report highlights a surge in imports during early 2025 as companies front-loaded shipments to preempt tariff hikes. However, with effective tariff rates peaking at 17.5% in Q2 2025 and expected to decline to 5.0% by mid-2026, trade volumes may contract later this year. This uncertainty is challenging industrial occupiers, particularly those reliant on import-driven logistics.

Source: Cushman & Wakefield Research.

Retail and industrial sectors are most exposed to tariffs, as higher costs pressure supply chains and consumer spending. The report suggests that even if tariffs ease, the lingering uncertainty will dampen demand for warehouse and distribution spaces in the near term. For example, rightsizing among e-commerce providers, which began in 2023, has reduced demand for large-scale fulfillment centers. However, the long-term outlook is brighter, with manufacturing activity—bolstered by recent investments in production facilities—creating a foundation for sustained industrial demand.

Occupiers can mitigate risks by diversifying supply chains, leveraging third-party logistics providers (3PLs) to enhance flexibility. Investors should focus on markets with strong manufacturing bases, such as the Southeast and Midwest, where industrial fundamentals are supported by secular trends like nearshoring. The report’s baseline scenario assumes trade tensions will ease, but downside risks remain, particularly if tariffs escalate further (e.g., reaching 27.6% in the worst-case scenario). Strategic planning and market selection will be critical for navigating this volatility.

Conclusion:

The industrial real estate market in 2025 is at a crossroads, balancing short-term challenges with long-term opportunities. While demand softens and vacancies rise, the sector’s fundamentals are buoyed by supply constraints and manufacturing growth. Investors and occupiers must stay agile, capitalizing on softer rents and strategic locations while preparing for a potential rebound in 2026.

How all this will impact us in the Greater Toronto Area and Southern Ontario remains to be seen; pending headwinds such as trade negotiations, business competitiveness, and consumer demand. Stay tuned for Part 2, where we’ll explore capital market trends and strategies for optimizing industrial portfolios in this dynamic environment.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com