Establishing True Valuations Across Differing Markets

August 15th, 2025

The most common questions among those deep in the industrial real estate market likely fall into the general pattern of “Where in the cycle are we?”

Or, “Have we hit the bottom yet?”

Or even, “When will things turn around?”

Because for the past several years now, the broader economic landscape has been marred by uncertainty. First it was the economic lockdowns, then the brief but spectacular boom in logistics and e-commerce; followed closely by supply chain bottlenecks and rising prices, and the resulting sharp increase in interest rates.

Since that initial wave of blockbuster deals and a behemoth pipeline of new inventory, things have trailed off, with a flurry of sublets, delayed projects, and a general mismatch in expectations between Buyers and Sellers; Landlords and Tenants.

Not that we needed it, but other headwinds, such as global conflicts and tariffs and trade talks have only made things less certain – with scores of businesses pushing off decisions while capital sat on the sidelines.

Transactions still took place, as they always do. People can’t wait forever. Yet overall confidence never really materialized that we were going to take another run into the next upswing.

That all said, it does feel like the market has probably come close to or already reached a bottoming out. Perhaps not in every submarket or asset class, nor for every class of property. But value plays are slowly popping up.

And those who were either priced out or who refused to partake in what they perceived were top-of-market valuations – the same groups who bought land at $500,000 per acre or $120 PSF – have now come out looking to redeploy capital and make their next moves.

Likewise, businesses that focused on efficiencies and operating profits might look to take advantage of stabilized rents and values to scoop up good deals for the next 5, 10, or 15 years. Everything always moves in cycles. It’s not quite certain where we currently sit, although for the first time in a long time, it feels as if the broader market is holding steady, albeit in the same cautious way.

So without further ado, let’s examine how each of the Greater Toronto Area regions performed in Q2 2025, and where we expect the market to go moving forward.

Key Takeaways from Q2 2025 – Toronto East Markets

- The availability rate decreased from 8.9% to 7.0%, with 6.9% available for lease and 0.1% available for sale;

- We had 862,442 SF of new supply year-to-date and 1,333,787 SF still under construction;

- We had 1,055,188 SF of absorption; and

- The weighted average asking net rent was $13.82 PSF, down from $15.50 PSF the previous quarter, with additional rent of $3.46 PSF (a decrease from $3.49 PSF).

Why are the GTA East Markets in such demand?

Generally, the Toronto-East markets have strong economics – relatively inexpensive land compared to other markets in the GTA, better availability of land, better located industrial land with proximity to the City, relatively low development charges, and great access to major highways.

We have seen a number of major Users and Developers step in and make commitments on large pieces of land for spec development and design build, which amounts to millions of square feet being built and in the pipeline.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

This week we are covering the Toronto-East Markets

(Pickering, Ajax, Whitby, Oshawa & Clarington)

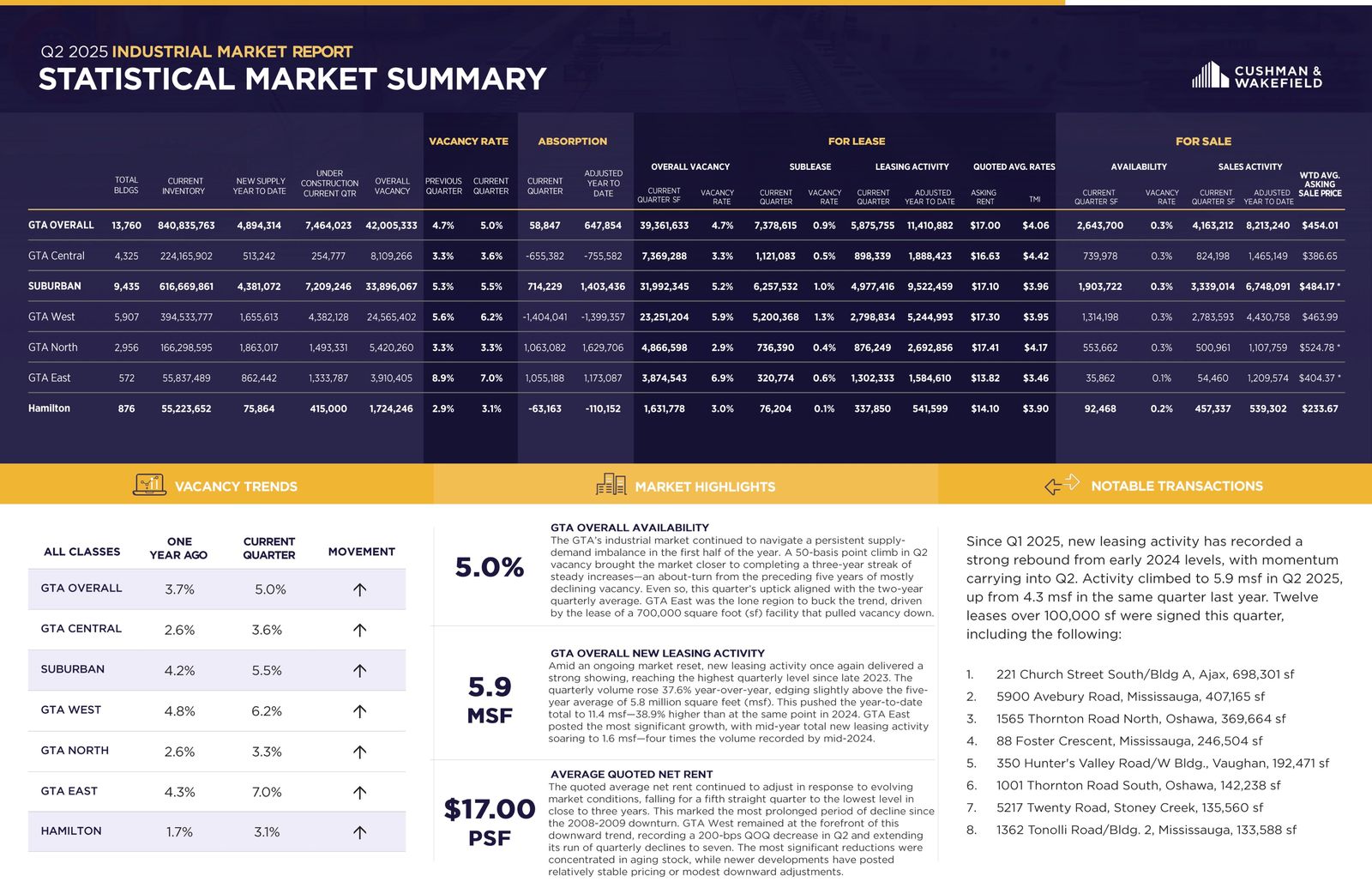

Statistical Summary – GTA East Markets – Q2 2025

Q2 2025 GTA Industrial Market Overview – Source: Cushman & Wakefield

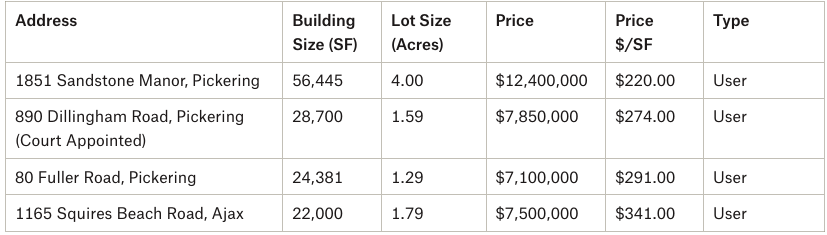

Properties Sold between April 2025 – June 2025, from 20,000 SF plus

80 Fuller Road, Pickering.

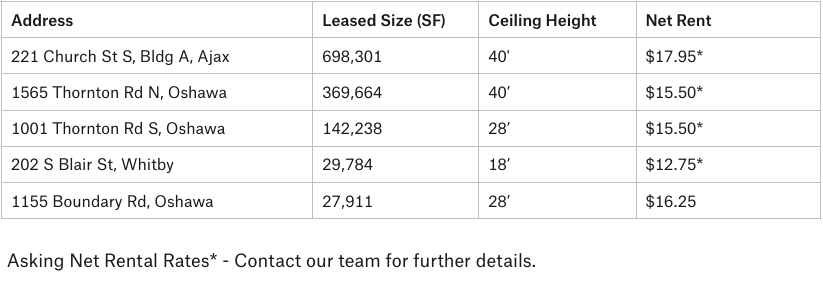

Properties Leased between April 2025 – June 2025, from 20,000 SF plus

221 Church St S, Bldg A, Ajax.

Major Development Projects Ongoing in GTA East Markets

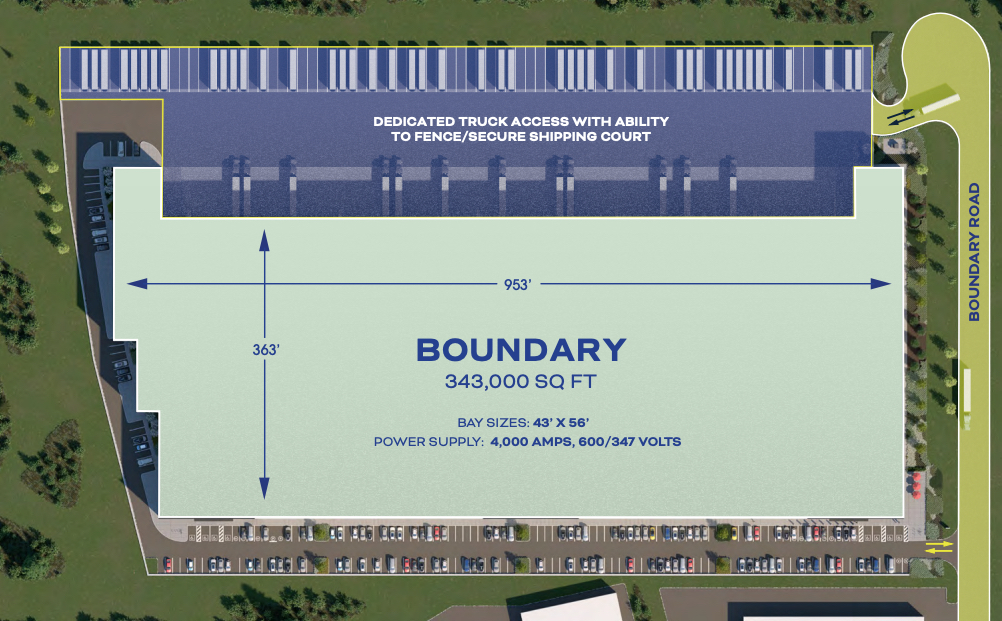

1. Carttera – 1900 Boundary Road, Whitby

1900 Boundary Road, Whitby. Source: Colliers.

1575 Clements Road, Pickering. Source: Colliers.

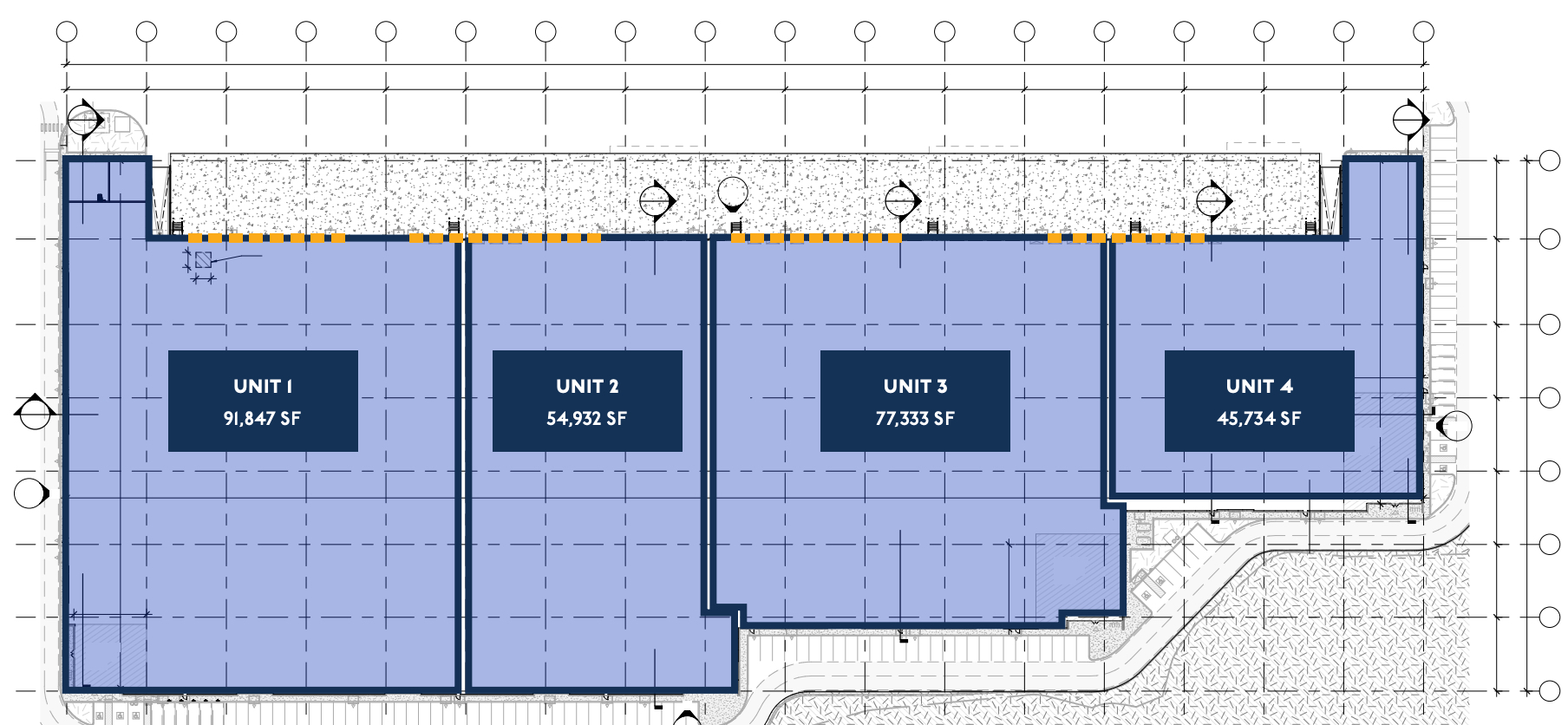

Triovest is constructing a 270,163 SF facility at 1575 Clements Road in Pickering. Situated on approximately 22 acres of land, the property will boast a 40’ clear height with 36 truck-level and 2 drive-in doors, 1,600 amps of heavy power and a 130’ truck court. Expected delivery is Q2 2025 with flexible configurations starting at 45,734 SF. Colliers is currently marketing the asset for lease.

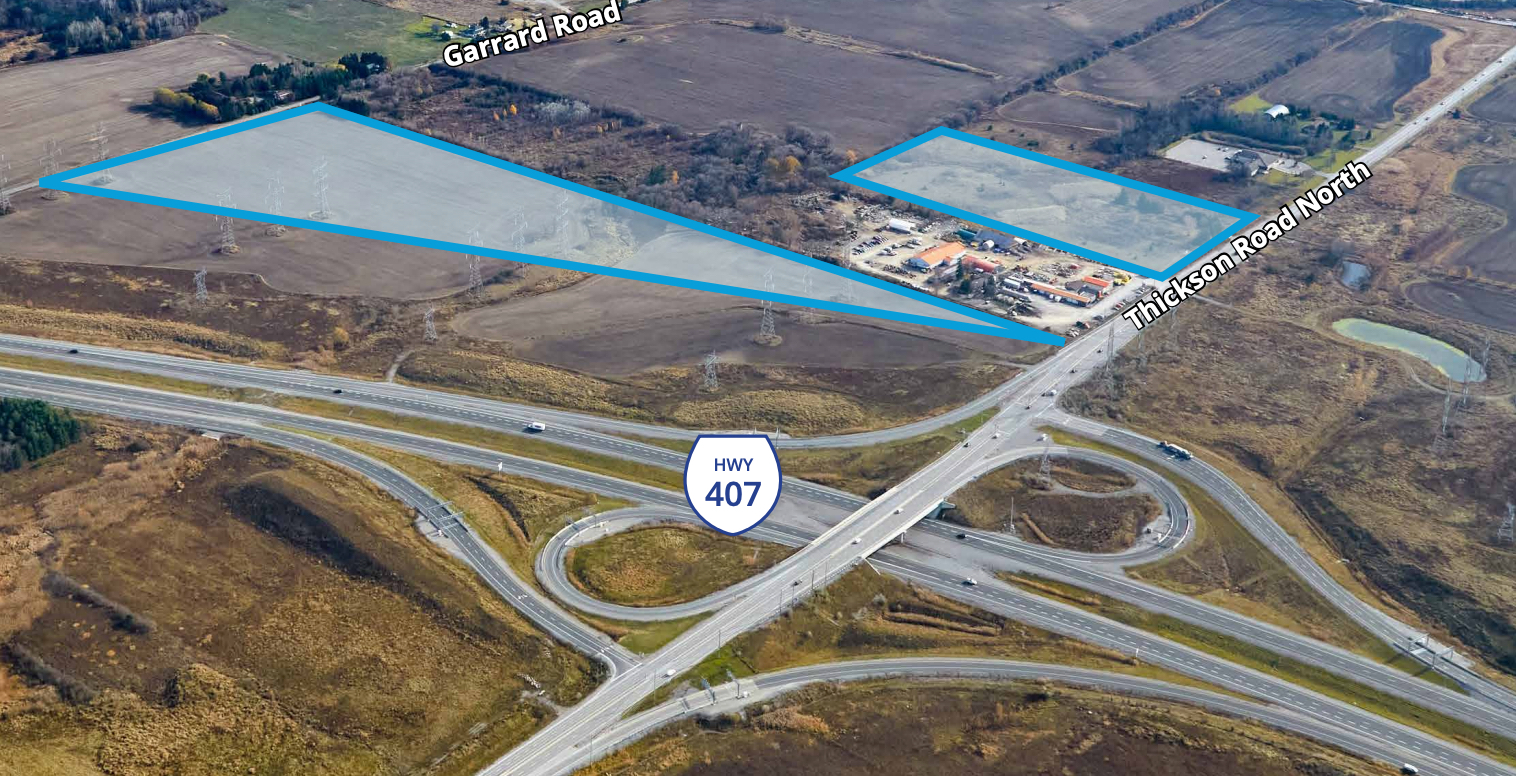

3. Rosewater Group – 5385 Thickson Rd N & Garrard Rd, Whitby

5385 Thickson Rd N & Garrard Rd, Whitby. Source: Colliers and D’Orsay + Co.

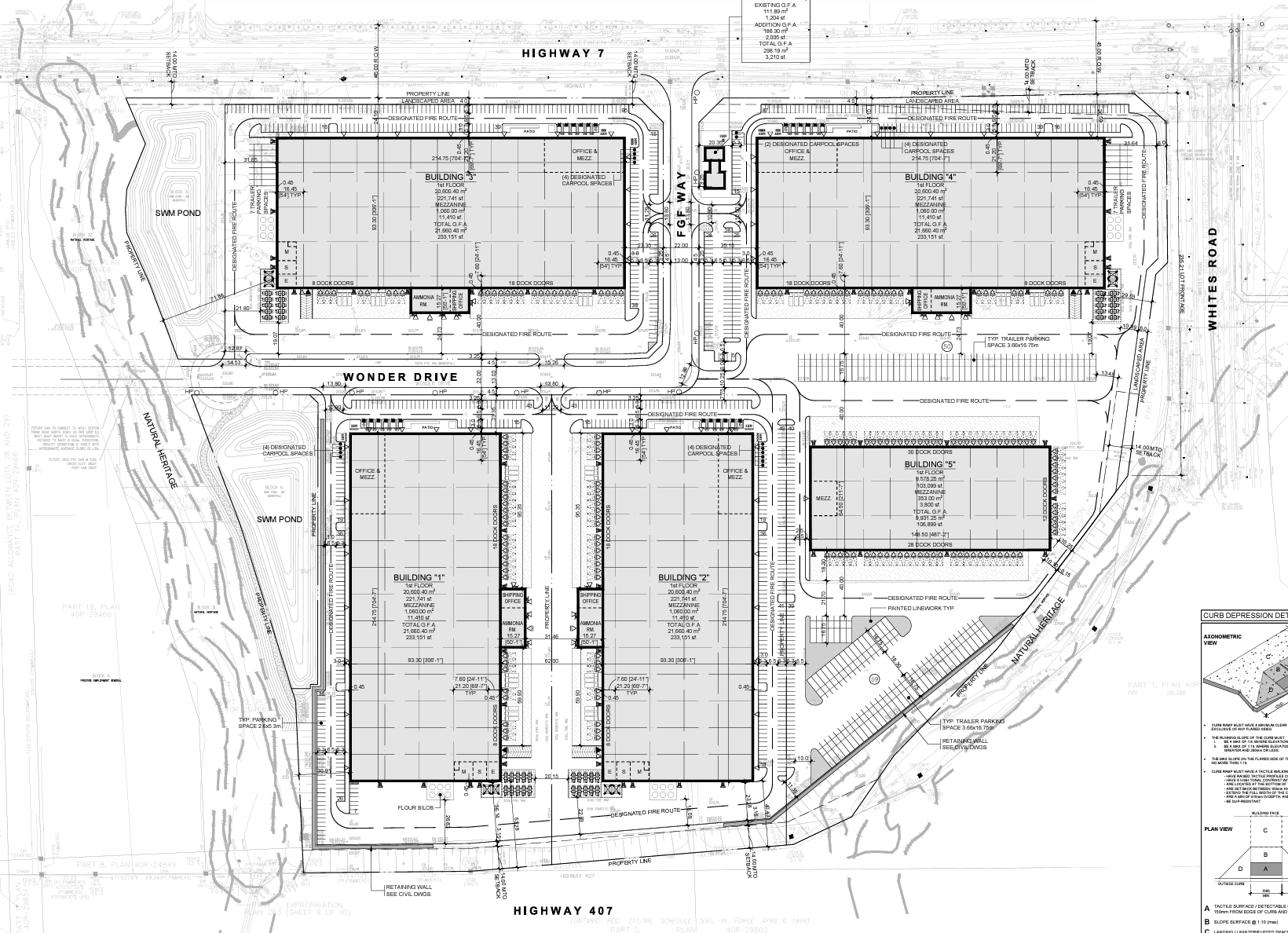

FGF Brands, with Caplink as the partner developer, is constructing the “FGF Food Manufacturing Campus” (also known as the “Wonderbrands Innovation Business Park”) at 745-815 Highway 7 in Pickering, ON.

The six-building industrial and office development sits on 151 acres and will total over 1-million square feet upon completion; the largest food manufacturing campus in the GTA and one of the most cutting-edge in terms of technology with robotics, integrated AI systems, machine learning, and supply chain innovations.

The park will host approximately 3,000 new employees and will potentially see Wonder Bread, D’Italiano, Country Harvest, Casa Mendosa, Gadoua, Stonefire, and other FGF-brand products manufactured and distributed through its doors.

- Building A will be 436,650 SF with 60 truck-level and 4 drive-in doors.

- Building B will be 616,268 SF with 106 truck-level and 8 drive-in doors.

- Building C will be 385,770 SF with 52 truck-level and 4 drive-in doors

- Building D will be 75,865 SF with 11 truck-level and 2 drive-in doors.

- Building E will be 56,886 SF with 12 truck-level and 2 drive-in doors.

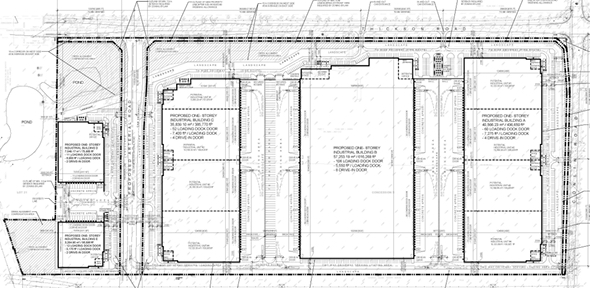

Fieldgate Commercial Properties and First Gulf are constructing the Brooklin Gate Business Park in Whitby, Ontario. With occupancy expected in Q3 2025, the 311,680 square foot warehouse offers a 40 foot clear height, and 52 truck-level and 2 drive-in doors. Colliers is marketing the asset for lease.

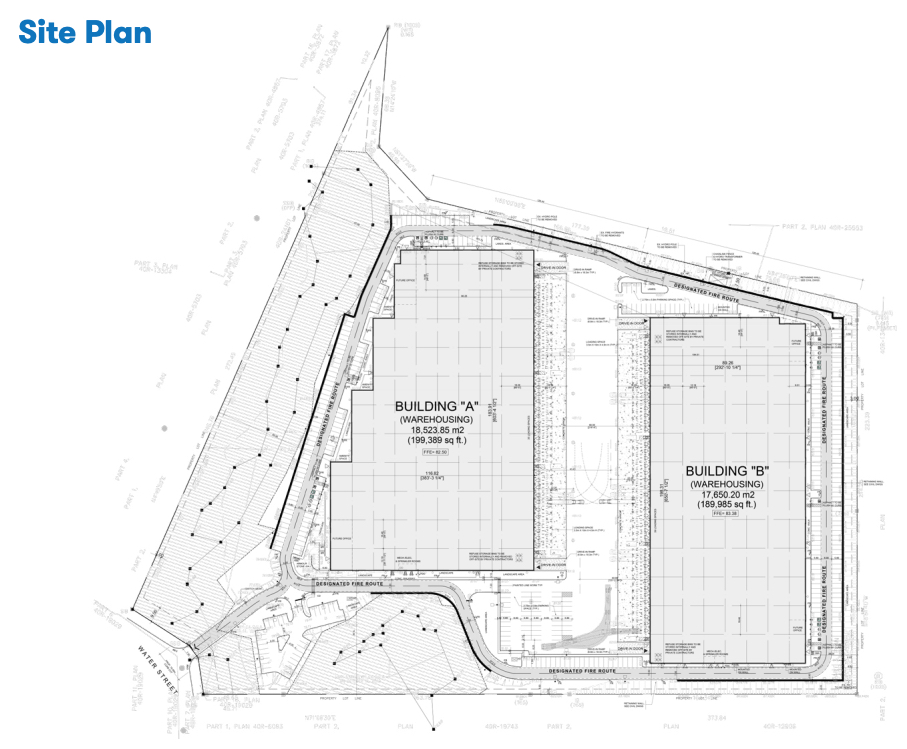

7. Dream REIT – 220 Water Street, Whitby

220 Water Street, Whitby. Source: Avison Young.

Dream REIT is developing two speculative industrial buildings totalling up to 389,374 SF. Located minutes from Highway 401, the properties will offer 40’ clear heights with 1,600 amps of heavy power and a 60’ staging bay. Building A will be 199,389 SF in size with 35 dock doors and 2 drive-in doors. Meanwhile, Building B will be 189,985 SF with 39 docks and 2 drive-in doors. Avison Young is marketing the project.

What Lies Ahead:

- Rental Rates: The Toronto-East markets have a weighted average rental rate of $13.82 PSF net, the lowest across the GTA regions. Rents have fallen over the past 12 months and are beginning to stabilize just as vacancies have from their crest of 8.9% last quarter. Likewise, annual rental escalations have decreased but remain steady between 3 – 3.5%. Leasing is slower and it is taking longer to complete a deal, with the recent tariffs not helping to move things forward. Finally, increased vacancies have provided Tenants with more options, putting downward pressure on rents, specifically in Class B or C industrial buildings. Overall, we are in a relatively balanced market between Landlords and Tenants.

- Property Values: The Toronto-East markets typically have the lowest weighted-average asking sale price in the GTA. As rental rates decrease in certain properties, we have seen a decrease in the value of investment properties. For users, we expect to see values remain elevated as supply is extremely limited. Finally, due to the overall softening of the market and slowdown in new construction, the value of development land has decreased.

- Development Opportunities: We saw a large number of completions in the East over the last 2-3 quarters, as well as a spike in vacancies – both of which bounced back in Q2 2025. Big players such as Panattoni, Nicola, Carttera, Crestpoint, PIRET, etc. (to name a few) are all involved… Development projects will continue, however, at a slower pace until absorption remains steady, most likely until at least 2026.

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation. And with our rental rates and valuations at all-time highs, and vacancy rates low, finding the right property is a real challenge.

Having said that, a lot of transactions are being done off the market.. and to participate in that, you should connect with experienced brokers that have long-standing relationships with property owners.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com