Establishing True Valuations Across Differing Markets

April 16th, 2021

Spring is finally upon us, and despite the sunny outlook and promising signs of global recovery, the Greater Toronto Area is still dealing with the aftermath of a dark winter. Specifically, we have found ourselves in yet another lockdown. Only this time around, all non-essential goods at retailers such as WalMart, Sam’s Club, and Costco have been blocked off, forcing consumers to purchase all of their non-food or medical-related items online.

While this may not seem like much… and while it may not be a huge inconvenience to us as customers of these establishments… this small policy change may have increased household online order volume by a factor of two or three, overnight. Where we once delivered a full carload of supplies home, a sizeable portion must now be picked off warehouse shelving elsewhere (essentially, duplicate inventory) and shipped via freight, LTL truck, or last-mile delivery vans.

Multiply this effect over millions of households in Southern Ontario and you get an even further strained supply chain and logistics network.

So what does this mean in the context of the industrial market?

Well, for a market that was already at sub-2% availabilities for 11 straight months, it means the competition for industrial space will only increase.

Retailers hoping for everything to re-open by May or June might finally be convinced that an e-commerce pivot (or add-on) is necessary to survive. Grocery delivery services are naturally blossoming and eating up dry and cold storage space. And 3PLs are swallowing up inventories at a torrid pace while maturing and diversifying their services with flexible offerings such as ‘warehousing on-demand.’

And so, we find ourselves back where we seem to always be.

New sectors and applications for industrial bolstering demand… And still no answer to the issue of a chronic lack of space.

Key Takeaways from Q1 2021 – Toronto Central Markets

- The availability rate decreased from 1.8% to 1.6%, with a lease availability rate of 1.4% and a sale availability rate of 0.2%;

- We had 1,692,703 SF under construction;

- We had 859,458 SF of absorption;

- The weighted average asking net rent was $10.43 PSF, up from $9.68 the previous quarter, with additional rent of $3.68 PSF; and

- The weighted average asking sale price was $165.18 PSF.

Interesting Development

We had reported on the conversion of the old Campbell’s soup factory in a previous report last year. However, now, the project is finally underway and the demolition of the previous facility has been completed; with construction beginning soon.

For more information on this exciting project visit www.60birmingham.ca

Why are the GTA Central Markets in such demand?

Is it proximity to labour and a higher population density, and thus, a reduction in transportation cost? Or is it savings in development charges vs 905 areas, proximity to major transportation nodes, highways, public transportation, etc?… Or all of the above?

Well, one thing is for certain, the Toronto-Central Markets are highly sought-after by both Investors and Occupiers of commercial real estate and is an environment worth exploring for opportunities.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

In order to get to the truth, we need to dig a bit deeper…

This week we are covering the Toronto Central Markets (Toronto, North York, Etobicoke & Scarborough)

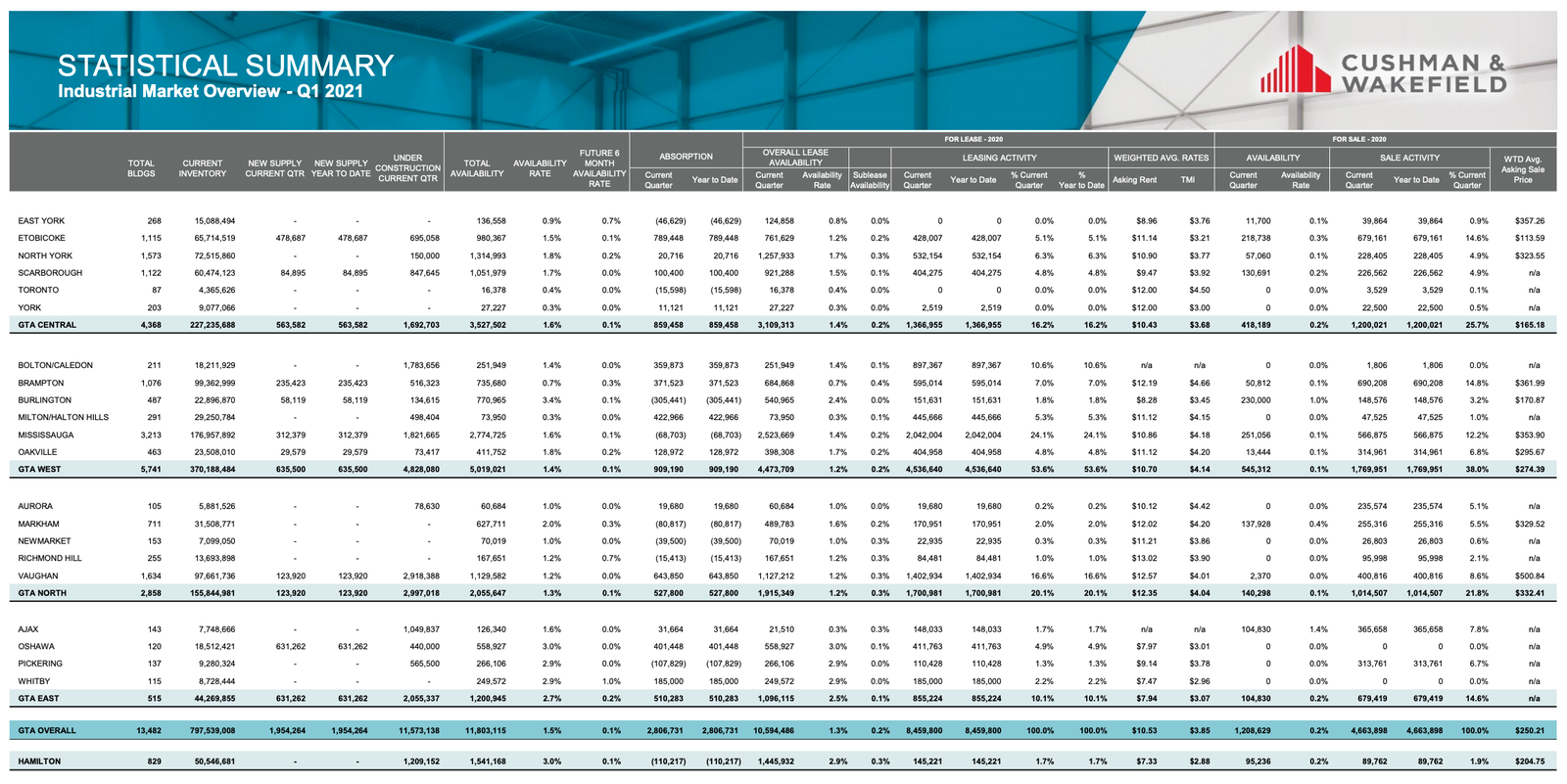

Statistical Summary – GTA Central Markets – Q1 2021

Q1 2021 GTA Industrial Market Overview – Source: Cushman & Wakefield

Q1 2021, Industrial Market Overview – Source: Cushman & Wakefield

GTA Central Markets (Scarborough)

Properties Sold between January 2021 – March 2021, from 20,000 SF plus

44 Milne Avenue, Scarborough

GTA Central Markets (Scarborough)

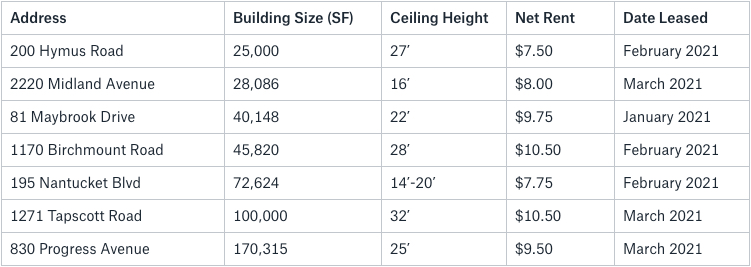

Properties Leased between January 2021 – March 2021, from 20,000 SF plus

830 Progress Avenue, Scarborough

GTA Central Markets (North York)

Properties Sold between January 2021 – March 2021, from 20,000 SF plus

In the North York Sub-Market in Q1 2021, a total of 6 properties were sold (429,158 SF); 4 were investment sales and two were user sales. The prices achieved were in the range of $144 PSF – $247 PSF, with an average building size of 71,526 SF and an average price of $185.83 PSF.

15 Leswyn Road, North York

GTA Central Markets (North York)

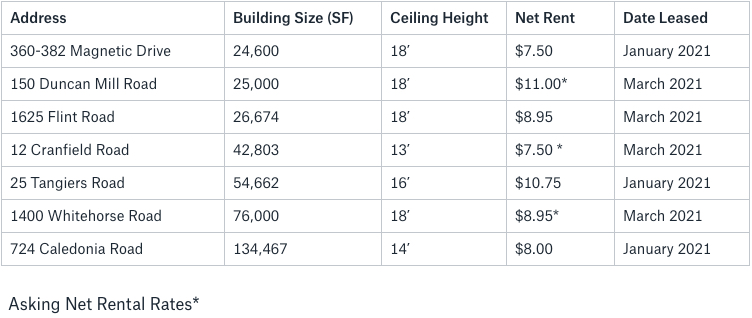

Properties Leased between January 2021 – March 2021, from 20,000 SF plus

724 Caledonia Road, North York

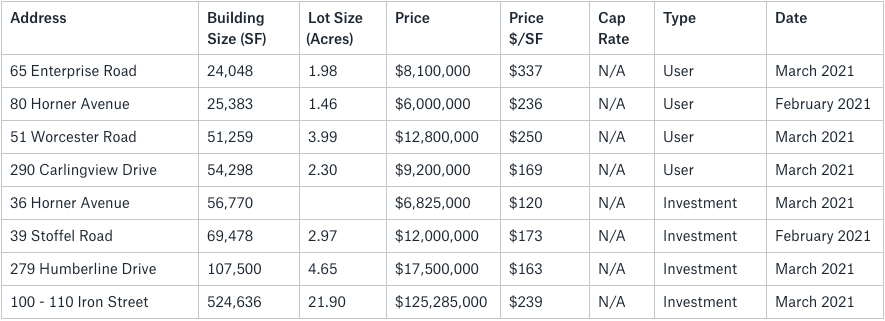

GTA Central Markets (Etobicoke)

Properties Sold between January 2021 – March 2021, from 20,000 SF plus

100 – 110 Iron Street, Etobicoke

GTA Central Markets (Etobicoke)

Properties Leased between January 2021 – March 2021, from 20,000 SF plus

161 The West Mall, Etobicoke

- Rental Rates: We have seen a further increase in net rental rates across the board into double-digit territory, depending on a number of factors, such as building size, location, ceiling height, etc. Based on the increase of value of industrial land, infill sites, construction costs, etc… we can only see these rates continue to grow. Overall, we are still in a Landlord’s market.

- Property Values: It really depends on the building size and location. Buildings between 20k and 50k SF are selling north of $300 PSF… and if there is any redevelopment potential, we are seeing transactions north of even $400 PSF, again, depending on size and location. CAP rates are still somewhere between 4.5% to 4.75% but it really depends on the rental rates in place. If we have older rental rates with immediate growth potential, then CAP rates could end up below 4%.

- Development Opportunities: Looking across the Toronto-Central markets, there is still great interest from developers to purchase infill sites and redevelop older and obsolete industrial buildings to newer, modern distribution centres. A good example is 60 Birmingham, which we mentioned earlier. Given its central location and proximity to major highways and labour, larger industrial sites in the Toronto-Central markets will continue to be in great demand.

Conclusion:

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation. And with our rental rates and valuations at all-time highs, and vacancy rates low, finding the right property is a real challenge.

Having said that, a lot of transactions are being done off the market.. and to participate in that, you should connect with experienced brokers that have long-standing relationships with property owners.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 25 years.

Goran Brelih is a Senior Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 27 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Goran is currently serving as Immediate Past President of the SIOR ‐ Society of Industrial and Office Realtors, Central Canadian Chapter.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield is a leading global real estate services firm that delivers exceptional value by putting ideas into action for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with 48,000 employees in approximately 400 offices and 70 countries.

In 2017, the firm had revenue of $6.9 billion across core services of property, facilities and project management, leasing, capital markets, advisory, and other services. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Senior Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Immediate Past President, SIOR – Central Canada Chapter

www.siorccc.org

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com