Q1 2023 Insight, Toronto-Central Markets

Establishing True Valuations Across Differing Markets

April 28th, 2023

We continue to trod along in what may seem like the ‘Twilight Zone.’

Tuning into discussions and reading about the state of the markets, many stakeholders and brokers seem to be waiting for the other shoe to drop.

There is no doubt about it – things have gotten tougher in many aspects of daily and business life. The cost of living has increased, as has the cost of doing business. Borrowing has more of a bite to operators. And the industrial market has slackened slightly, with close to a million square feet of negative absorption in the GTA Central markets in Q1 2023. As a result, landlords and developers are keeping a close eye on whether competing availabilities may have an impact on lease negotiations or new product coming online.

That said, owners and occupiers are still incredibly active. Significant deals are closing on a regular basis. Major tenants are pushing through expansion plans. And those looking for space still complain of the difficulty in securing it; whether for lease or for purchase.

One lens with which to view this market is more of a restructuring or completion of a market cycle, more than anything else. Retailers such as Bed, Bath & Beyond have announced the closing of their operations across Canada, just as others are looking to break into the market from south of the border. And on the investment side, continued concerns in office and retail will only drive more capital into the now favoured industrial class.

Those that made strategic moves in the years leading up, whether through e-commerce adoption, asset re-allocation, logistics networks, or otherwise, are now able to reap the benefits.

Overall, while we do see this re-shuffling occurring, the GTA industrial market is incredibly well-positioned and insulated from the noise.

So with that said, let’s examine how each of the Greater Toronto Area regions performed in Q1 2023, and where we expect the market to go moving forward.

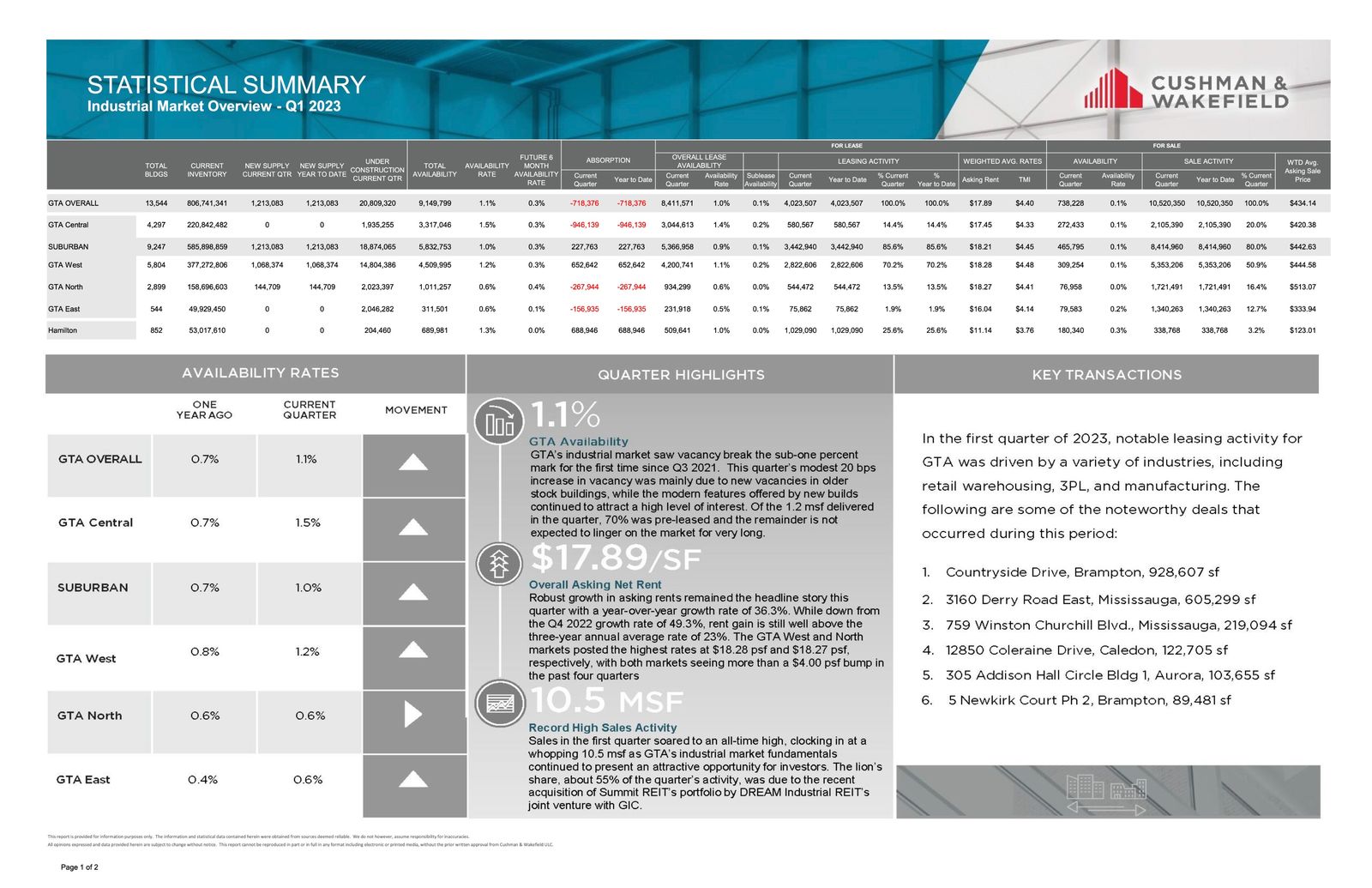

- The availability rate increased from 1.1% to 1.5%, with a lease availability rate of 1.4% and a sale availability rate of 0.1%;

- We had 1,935,255 SF under construction;

- We had 946,139 SF of negative absorption;

- The weighted average asking net rent was $17.45 PSF, down from $17.65 the previous quarter, with additional rent of $4.33 PSF; and

- The weighted average asking sale price was $420.38 PSF.

Why are the GTA Central Markets in such demand?

Is it proximity to labour and a higher population density, and thus, a reduction in transportation cost? Or is it savings in development charges vs 905 areas, proximity to major transportation nodes, highways, public transportation, etc?… Or all of the above?

Well, one thing is for certain, the Toronto-Central Markets are highly sought-after by both Investors and Occupiers of commercial real estate and is an environment worth exploring for opportunities.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

This week we are covering the Toronto Central Markets (Toronto, North York, Etobicoke & Scarborough)

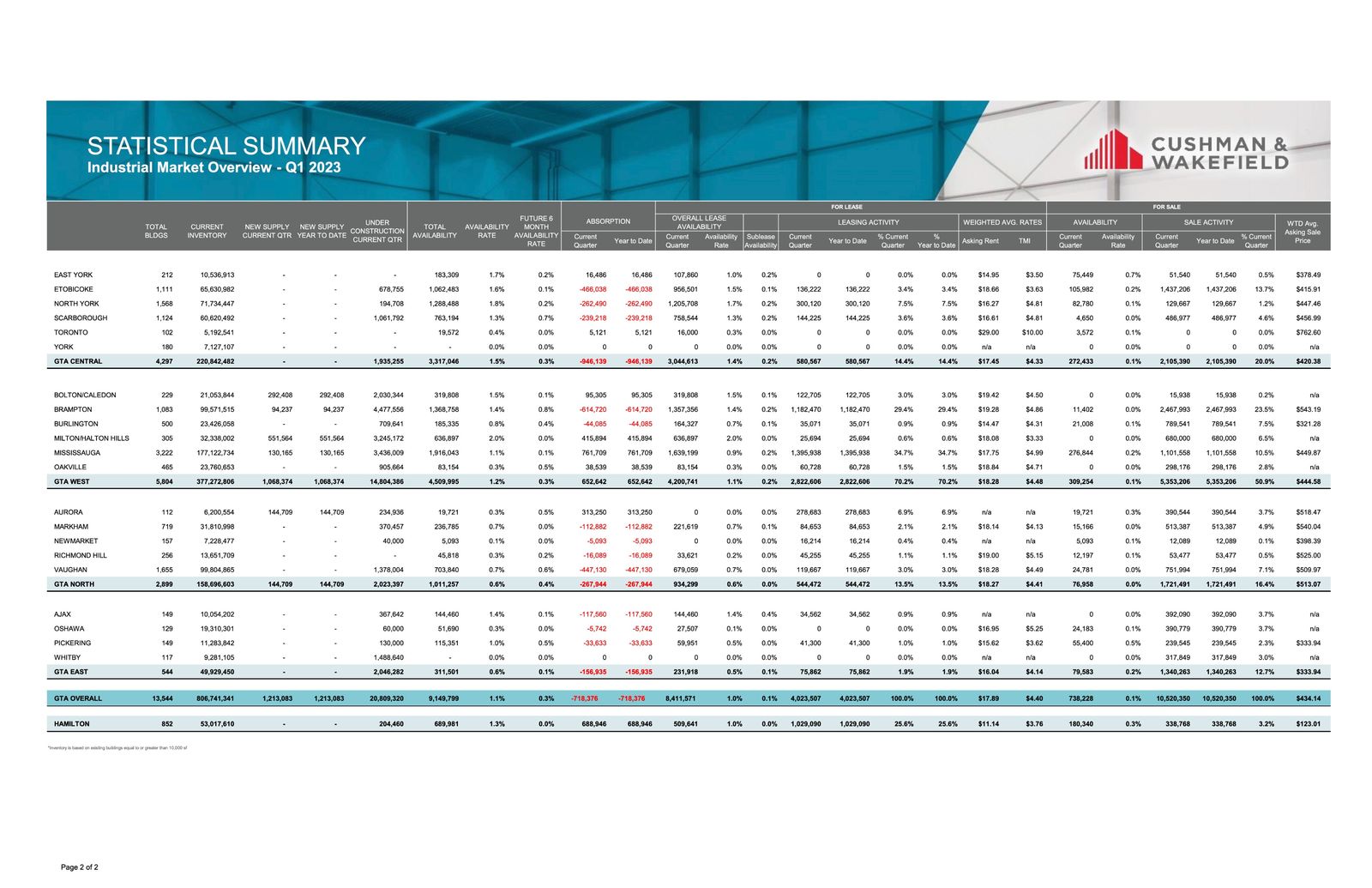

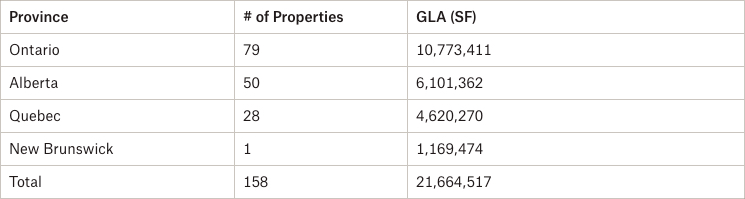

Statistical Summary – GTA Central Markets – Q1 2023

Q1 2023 GTA Industrial Market Overview – Source: Cushman & Wakefield

Q1 2023, Industrial Market Overview – Source: Cushman & Wakefield

GTA Central Markets (Scarborough)

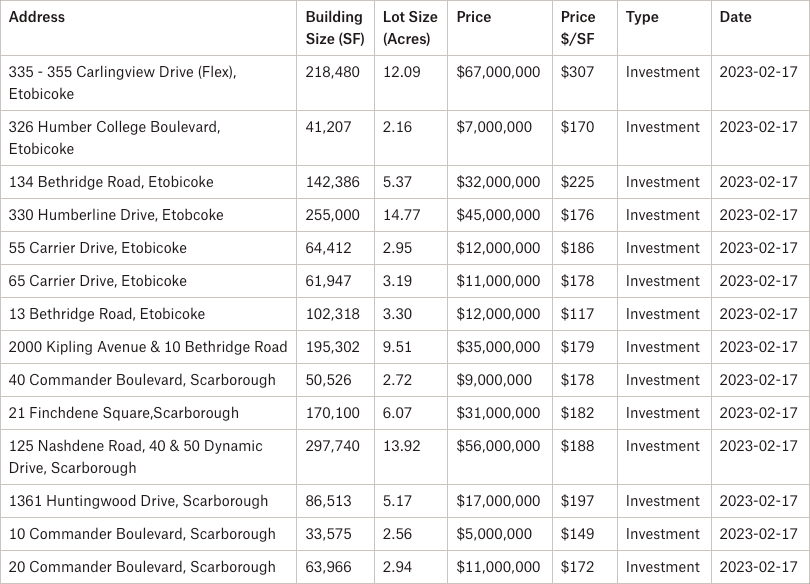

Properties Sold between January 2023 – March 2023, from 20,000 SF plus

41 Lamont Avenue, Scarborough

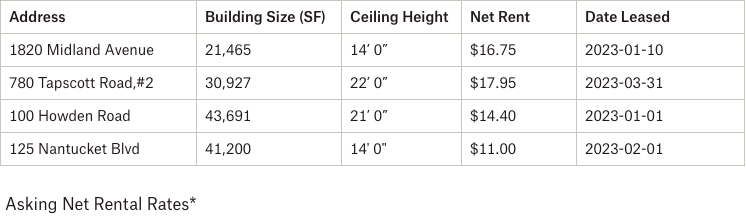

Properties Leased between January 2023 – March 2023, from 20,000 SF plus

100 Howden Road, Scarborough

Properties Sold between January 2023 – March 2023, from 20,000 SF plus

10 Tempo Avenue, North York

Properties Leased between January 2023 – March 2023, from 20,000 SF plus

135 Wendell Avenue, North York

330 Humberline Drive, Toronto

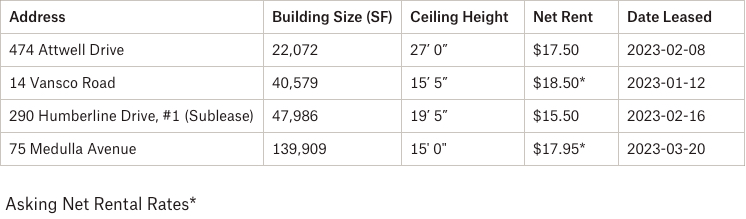

Properties Leased between January 2023 – March 2023, from 20,000 SF plus

75 Medulla Avenue, Etobicoke

Portfolio Sale

- Rental Rates: We continue to see a general upward pressure across the board into the high-teens – and even low-twenties – PSF net, depending on a number of factors, such as building size, location, ceiling height, etc. Based on the increase of value of industrial land, infill sites, construction costs, etc… we will see these rates continuing to grow. Overall, we are still in a Landlord’s market, however, the negative absorption of close to a million square feet in the Central Markets in Q1 2023 has pushed lease availabilities to 1.4%. If this trend continues, we may begin to see a shift to a more balanced market. In this case, higher construction and maintenance costs may be passed through in the form of stronger additional rents (TMI).

- Property Values: We have seen a decrease in value in some properties that have been taken to the market at new watermark values. That said, depending on the building size and location, and especially for Class A, well-located space, pricing shall remain strong. Given the most recent increases in interest rates, we will see a continued impact on CAP rates.

- Development Opportunities: Looking across the Toronto-Central markets, there is still great interest from developers to purchase infill sites and redevelop older and obsolete industrial buildings to newer, modern distribution centres, as well as industrial condos. Given its central location and proximity to major highways and labour, larger industrial sites in the Toronto-Central markets will continue to be in great demand.

Conclusion:

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation. And with our rental rates and valuations at all-time highs, and vacancy rates low, finding the right property is a real challenge.

Having said that, a lot of transactions are being done off the market.. and to participate in that, you should connect with experienced brokers that have long-standing relationships with property owners.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com