How Much Is Your Building Really Worth?

Establishing True Valuations Across Differing Markets

Q2 2020 Insight, Toronto-Central Markets

August 14th, 2020

This has been the full first quarter operating under COVID-19 and the resulting economic shutdowns. Obviously, events had a big impact on commercial real estate across the board, but it looks like, on the surface, that it wasn’t as tough on industrial. That being said, in order to understand what’s really going on, we need to go deeper and examine the various types of industrial real estate.

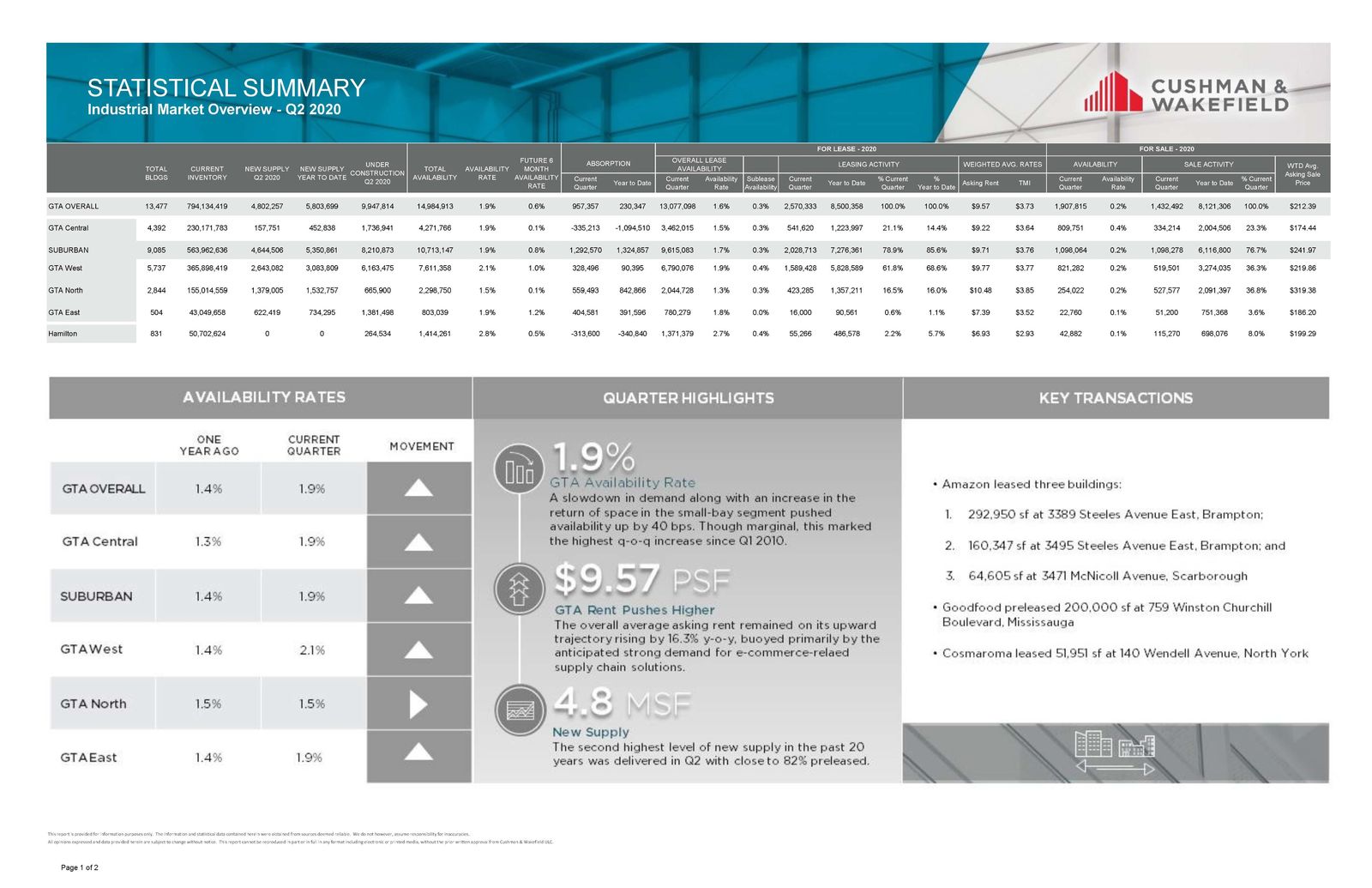

Our statistics show a relatively slight increase in the availability rate in Q2, going from 1.3% to 1.9%, and with a negative absorption of over 335,000SF. The hardest hit were smaller businesses and those that were forced to close. There was a lesser impact on medium to large-sized businesses, while e-commerce, warehousing, and distribution were firing on all cylinders.

Key Takeaways from Q2 2020

- Availability Rate rates increased from 1.3 % in Q1 2020 to 1.9% in Q2, with a lease availability rate of 1.5% and sale availability rate of 0.4%;

- We had 1,736,000 SF under construction;

- We had negative absorption of 335,000 SF;

- The weighted average asking net rent was $9.22 PSF with additional rent of $3.64 PSF; and

- The weighted average sale price was $174.44 PSF.

Interesting Announcements this Quarter

Purolator announced it will be opening a national super-hub in Etobicoke by 2021. The $330-million Etobicoke hub will be a 430,000-square-foot facility located on 60 acres of land across from Humber College, developed in line with Toronto’s Green Standard to ensure a sustainable site and building design. The hub is expected to triple the capacity of Purolator’s current network and utilize world-class automation technology, such as advanced robotics and sort containers, that will facilitate quicker and more efficient deliveries.

325 Humber College, Etobicoke

Why are the GTA Central Markets in such demand?

Is it proximity to labour and a higher population density, and thus, a reduction in transportation cost? Or is it savings in development charges vs 905 areas, proximity to major transportation nodes, highways, public transportation, etc?… Or all of the above?

Well, one thing is for certain, the Toronto-Central Markets are highly sought-after by both Investors and Occupiers of commercial real estate and is an environment worth exploring for opportunities.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

In order to get to the truth, we need to dig a bit deeper…

This week we are covering the Toronto Central Markets (Toronto, North York, Etobicoke & Scarborough)

Statistical Summary – GTA Industrial Market – Q2 2020

GTA Industrial Market Overview – Q1 2020 – Credit – Cushman & Wakefield ULC

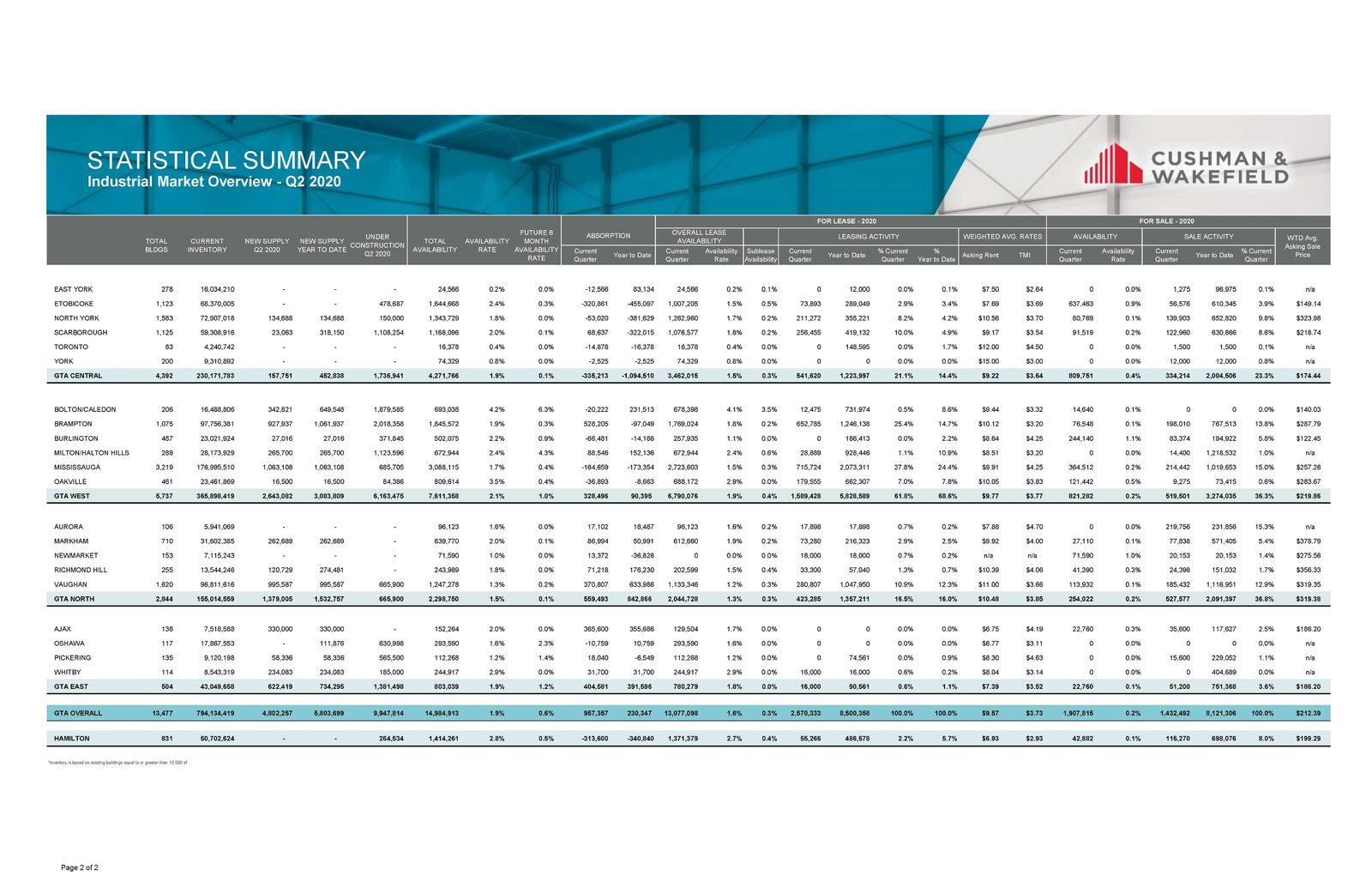

Statistical Summary – GTA Central Markets (Toronto, North York, Etobicoke & Scarborough), Q2 2020

So let’s take a closer look at how the different Toronto Central Markets performed during Q2 2020…

GTA Central Markets (Scarborough)

Properties Sold between April 2020 – June 2020, from 20,000 SF plus

In Q1 2020 in the Scarborough sub-market, 1 property was sold (24,600 SF). The price achieved was $3,430,000.

GTA Central Markets (Scarborough)

Properties Leased between April 2020 – June 2020, from 20,000 SF plus

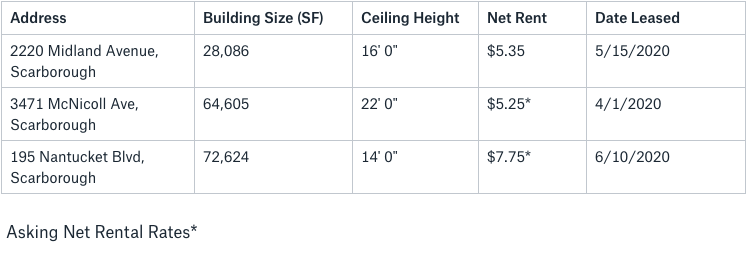

In the Scarborough sub-market in Q2 2020, a total of 3 properties were leased (165,315 SF). The net rental rates achieved were from $5.35 – $7.75 PSF, with an average building size of 55,105 SF and an average net rental rate of $6.12 PSF.

GTA Central Markets (North York)

Properties Sold between April 2020 – June 2020, from 20,000 SF plus

In Q1 2020 in the North York sub-market, 1 property was sold (21,638 SF). The price achieved is $199 PSF.

GTA Central Markets (North York)

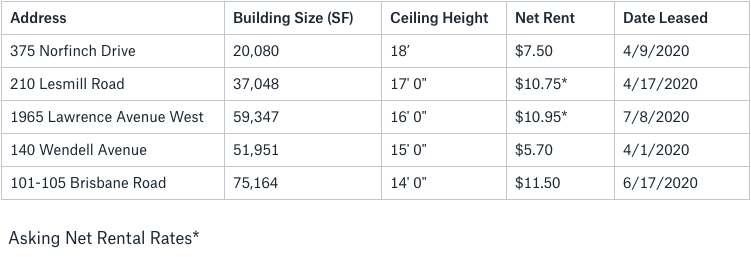

Properties Leased between April 2020 – June 2020, from 20,000 SF plus

In the North York sub-market, 5 properties were leased (totaling 243,590 SF) in Q2 2020. The net rental rates achieved were from $7.50 – $11.50 PSF, with an average building size of 48,718 SF and an average net rental rate of $9.28 PSF.

GTA Central Markets (Etobicoke)

Properties Sold between April 2020 – June 2020, from 20,000 SF plus

In the Etobicoke sub-market in Q2 2020, a total of 2 properties were sold (154,563 SF); 2 were user sales. The prices achieved were in the range of $149 – $200 PSF, with an average building size of 77,282 SF and an average price of $175 PSF.

GTA Central Markets (Etobicoke)

Properties Leased between April 2020 – June 2020, from 20,000 SF plus

In the Etobicoke sub-market, 2 properties were leased (totaling 45,446 SF) in Q2 2020. The net rental rates achieved were from $8.00 – $10.00 PSF, with an average building size of 22,723 SF and an average net rental rate of $9.00 PSF.

What Lies Ahead:

- Rental Rates: Not all real estate is created equal…. It is important to note that the Industrial asset class will weather this storm and come out strong, if not stronger than before… with the only exception potentially being small-bay properties. Increases in online retail sales, moving away from “just in time” inventory and relocating parts of manufacturing back to Canada from overseas (and including the production of PPE equipment) will continue to put pressure on industrial markets; keeping our rental rates steady and increasing, although maybe at a slower pace. Overall, we are still in a Landlord’s market and have a long way to go….

- Property Values: Multi-tenant industrial properties that are owned by private equity funds (and are highly leveraged) may see some difficult days ahead… we may see vacancy rates increase and maybe even CAP rates as well….. However, larger, single-tenant, logistics, warehouses and distribution facilities, and even manufacturing, should keep their values. A telling sign: those Landlords collected over 90% of their rents in April, May, and June 2020…

- Development Opportunities: There is not much land to be developed in the Toronto-Central Markets so we will continue to see infill redevelopment…

Conclusion:

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation. And with our vacancy rates, rental rates, and valuations having hit all-time highs right before COVID-19 took place, there may be plenty of opportunities to find creative solutions; whether it be through rightsizing, refinancing, bridge financing, sale-leasebacks, or otherwise.

While there may exist challenges in execution, Buyers are ever more hungry for product. Local, high-net-worth developers and investors are often active in bottom-of-market conditions. And well-capitalized institutional investors and pension funds are still willing to take a look at a deal if the numbers make sense.

Furthermore, a number of our clients are considering sale-leasebacks to re-capitalize their operations.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 25 years.

Goran Brelih is a Senior Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 27 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Goran is currently serving as Immediate Past President of the SIOR ‐ Society of Industrial and Office Realtors, Central Canadian Chapter.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield is a leading global real estate services firm that delivers exceptional value by putting ideas into action for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with 48,000 employees in approximately 400 offices and 70 countries.

In 2017, the firm had revenue of $6.9 billion across core services of property, facilities and project management, leasing, capital markets, advisory, and other services. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Senior Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Immediate Past President, SIOR – Central Canada Chapter

www.siorccc.org

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com