Q3 2020 Insight, Toronto-West Markets

Establishing True Valuations Across Differing Markets

November 13th, 2020

This has been the second quarter operating under COVID-19 and the resulting economic shutdowns. Obviously, events had a big impact on commercial real estate across the board, but it looks like, on the surface, that it wasn’t as tough on industrial. In fact, the growing trend of e-commerce has pushed industrial demand to new highs. Both warehousing and logistics, as well as cold-storage users have been snapping up space and creating an even more competitive environment.

The GTA West Industrial Markets are by far the largest industrial markets in the GTA, representing about 45% of GTA Industrial Inventory, or about 363,000,000 SF. The GTA West Markets were very active this quarter, with more than 6,220,000 SF under construction and a flurry of lease and sale transactions completed, as deals that were pushed back by the pandemic begin to close.

Key Takeaways from Q3 2020

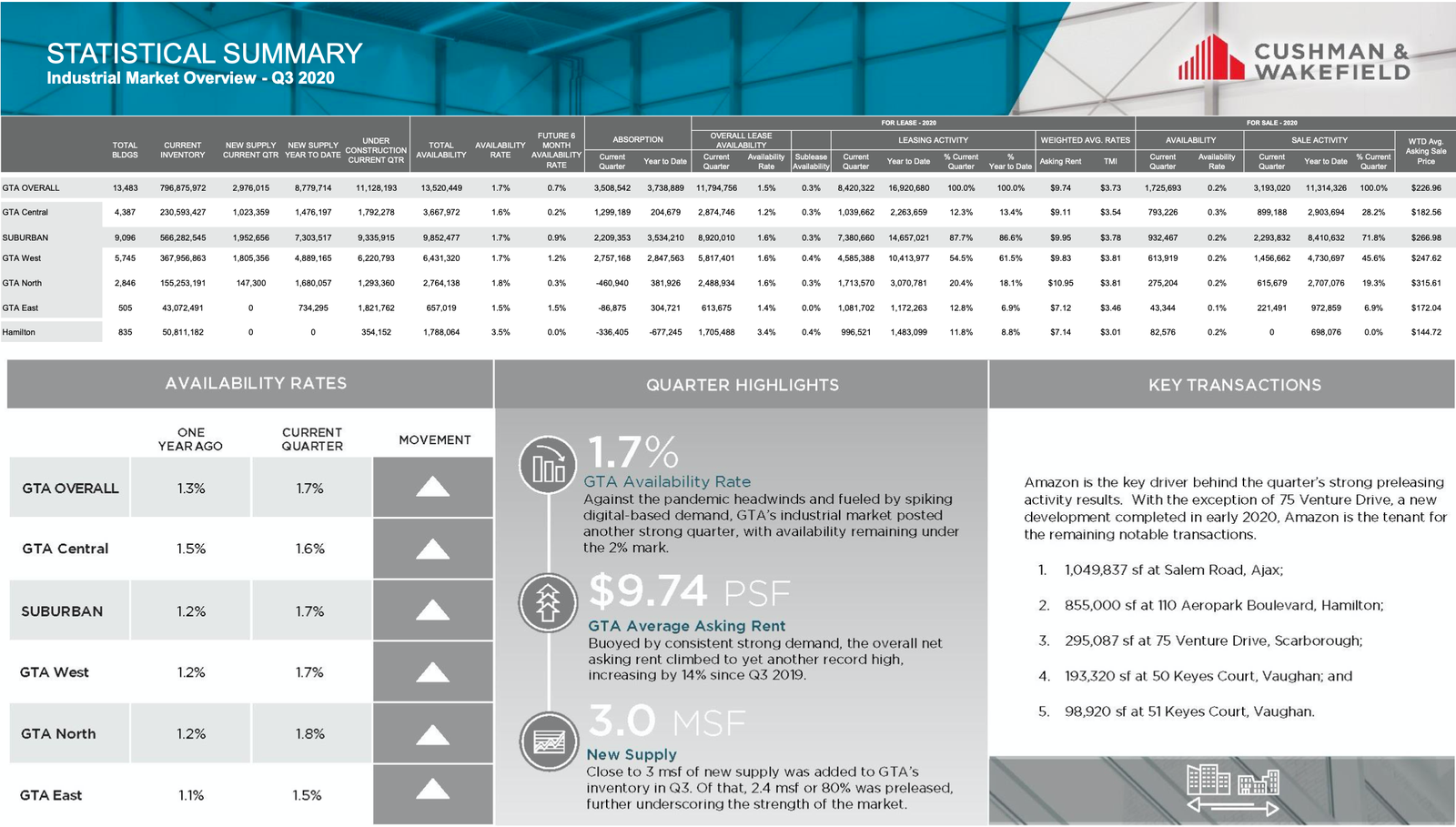

- The overall availability rate in the GTA-West Markets in Q3 2020 is 1.7%;

- Currently, there is about 6,220,000 SF under construction in the GTA-West Markets;

- The GTA West markets delivered 1.92 Million SF of new space to the market in Q3 2020;

- Absorption in Q3 2020 was 2.757 Milion SF;

- The City of Brampton Leasing Market achieved the highest net rental rates in Q3 2020 at $10.72, up from $10.12 PSF in the previous quarter, followed by the City of Mississauga with $10.31 PSF.

- Availability rate across GTA went slightly up to 1.7% in Q3 2020 from 1.5% in the previous quarter, while the weighted average net rental rates in GTA West markets reached $9.83 per SF; the second-highest in the GTA Industrial markets, behind only the GTA North Markets, while the weighted average sale price in the West markets was $247.62 per SF.

Interesting Announcement this Quarter

Another successful project completion by Panattoni Canada

Panattoni Canada announced the substantial completion of construction of a state-of-the-art distribution centre in Mississauga located at 2220 – 2260 Matheson Boulevard East. Prior to completion, the property was leased to a logistics company – Metro Supply Chain Group – on a long-term lease.

2220 – 2260 Matheson Blvd East, Mississauga

2220 – 2260 Matheson Blvd East, Mississauga

Features of the facility include 40-foot clear height, 35 truck level doors, 54’x50’ bay sizes, an ESFR sprinkler system, and 52 trailer parking stalls.

Panattoni Development Company (Canada) has been responsible for the new construction and re-development of over 12 million square feet of industrial buildings in Canada, including developments across the Greater Toronto Area in markets such as Brampton, Caledon, and Mississauga.

2260 Matheson Boulevard East offers unrivaled access for logistics needs in an area with extensive amenities and public transit offerings.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

In order to get to the truth, we need to dig a bit deeper…

This week we are covering the Toronto-West Markets (Mississauga, Brampton, Oakville, Milton, Caledon, Burlington & Halton Hills)

Statistical Summary – GTA West Industrial Market – Q3 2020

GTA Industrial Market Overview – Q3 2020 – Credit – Cushman & Wakefield ULC

So let’s take a closer look at how the Toronto West Markets performed during Q3 2020…

GTA West Markets (Mississauga)

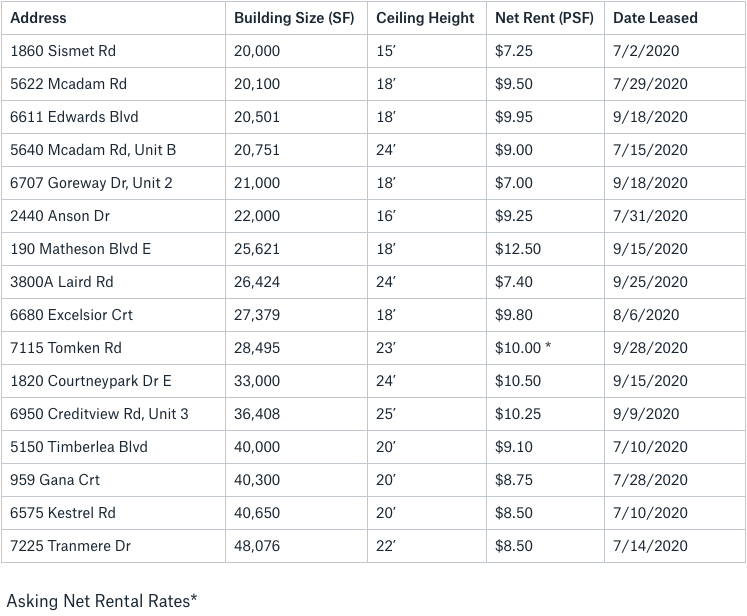

Properties Sold between July 2020 – September 2020, from 20,000 SF – 50,000 SF

6701 Financial Drive, Mississauga

2220 – 2260 Matheson Blvd East, Mississauga – Source: Panattoni

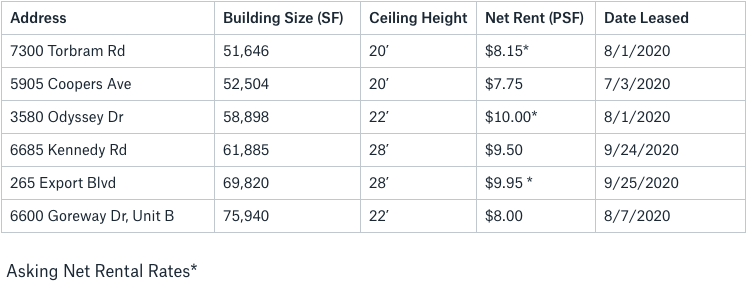

GTA West Markets (Brampton)

Properties Sold between July 2020 – September 2020, from 20,000 SF+

8995 Airport Road, Brampton

2675 Steeles Avenue West

GTA West Markets (Oakville)

Properties Sold between July 2020 – September 2020, from 20,000 SF+

No sales were done in this quarter.

In Oakville, a total of 3 properties were leased in Q3 2020 between 20,000 – 50,000 SF. The net rental rates achieved were from $10.00 – $10.52 PSF, with an average building size of 33,180 SF and an average net rental rate of $10.26 PSF.

Properties Leased between July 2020 – September 2020, from 50,000 SF – 100,000 SF

2323 Winston Park Drive

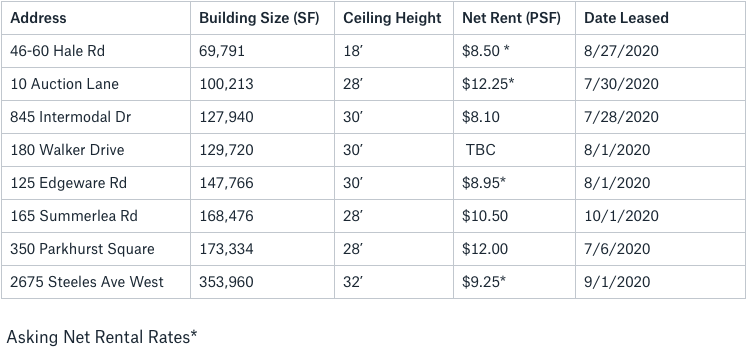

GTA West Markets (Burlington, Caledon, Milton, Halton Hills)

Properties Sold between July 2020 – September 2020, from 20,000 SF+

8100 Parkhill Drive

2800 Peddie Road, Milton

- Rental Rates: Currently at $9.83 per SF, the net rental rates are trailing behind the GTA-North Markets ($10.95 per SF). I expect these rental rates to remain at the same level or move slightly higher in the next quarter. The reason being, there is continued demand for large modern warehouse distribution space – which is being constructed in Toronto West Markets. That being said, we did see an increase in vacancy rates last quarter, which was mainly in the small to mid-bay market. And given the fact that small- and mid-size businesses were hit hard by the pandemic, this should not greatly impact rental rates since we are still in a Landlord’s market.

- Property Values: The weighted average asking sale price is about $247.62 per SF, which is considerably lower than in the GTA-North Markets (which trade at a weighted average of $315.61). I expect these prices to remain stable or to slightly increase…

- Development Opportunities: The GTA West Markets will continue to be the most active as far as development is concerned… in this quarter alone we had over 1.92 MSF completed, despite the existing roadblocks. A few important takeaways with respect to construction activity in GTA:

- New, modern, large, industrial, E-commerce space is in demand;

- Cold-storage space will be highly sought-after as food companies fight for distribution, as well as the need to store potential vaccines at frigid temperatures;

- It is a safe bet that the building of the future will be E-commerce facilities with 40’ clearance and with lots of parking for both cars and trailers…

- Costs are predicted to increase by at least 10% (for both labour and materials) and projects are expected to take 10% longer to construct…

- There are issues with sourcing some materials, specifically steel and concrete, and with more demand prices are going up;

- We are experiencing delays in the permitting process, inspections, and construction itself. Productivity is down as well (with fewer workers on projects, practicing social distancing);

- There is serious interest for most of the speculative large box buildings from E-commerce and food-related companies.

Conclusion:

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation.

And with our vacancy rates, rental rates, and valuations having hit all-time highs right before COVID-19 took place, there may be plenty of opportunities to find creative solutions; whether it be through rightsizing, refinancing, bridge financing, sale-leasebacks, or otherwise.

While there may exist challenges in execution, Buyers are ever more hungry for product. Local, high-net-worth developers and investors are often active in bottom-of-market conditions. And well-capitalized institutional investors and pension funds are still willing to take a look at a deal if the numbers make sense.

Furthermore, a number of our clients are considering sale-leasebacks to re-capitalize their operations.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 25 years.

Goran Brelih is a Senior Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 27 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Goran is currently serving as Immediate Past President of the SIOR ‐ Society of Industrial and Office Realtors, Central Canadian Chapter.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield is a leading global real estate services firm that delivers exceptional value by putting ideas into action for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with 48,000 employees in approximately 400 offices and 70 countries.

In 2017, the firm had revenue of $6.9 billion across core services of property, facilities and project management, leasing, capital markets, advisory, and other services. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Senior Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Immediate Past President, SIOR – Central Canada Chapter

www.siorccc.org

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com