Q3 2021 Insight, Toronto-East Markets

Establishing True Valuations Across Differing Markets

November 19th, 2021

“Only when the tide goes out do you discover who’s been swimming naked.”

- Warren Buffett

In good times, we are faced with an abundance of opportunities to grow and prosper. In the context of commercial real estate, this could mean investing in facilities for our operations, developing land to construct new buildings, or acquiring and leasing out properties.

Savvy investors and business operators always perform due diligence throughout the decision- and deal-making processes. However, in a strong and active market, there is relatively less uncertainty, and thus, less risk. Making moves is much more straightforward as there are more options to consider, with outcomes easier to predict and to forecast.

As we head towards winter, we find ourselves in a position fraught with question marks. Assumptions are being questioned and redefined. The underlying industrial market in the GTA is in an extreme imbalance, with many players chasing scarce inventory of land and properties. As a result, pricing is at all-time highs. And once secured, these assets are subject to economic forces, which themselves are far from normal.

Labour and material shortages (and cost inflation) continue to plague developers, who are working to orchestrate and time the construction process as they apply for permits and zoning – which have also been delayed. Industrial occupiers also feel the pinch as their leases renew or they look to expand. Nothing is guaranteed. And success comes at a premium.

Those who planned well in advance are reaping the rewards of having assets in place or the capacity to take on new business and more projects. Those who moved in reaction – or who were slow to adapt – are looking for new strategies to position themselves for the future.

Patience and readiness have become virtues for the modern GTA CRE professional. The patience to wait for opportunities. And the readiness to act upon them.

The current state will only continue to grow more competitive, with product harder to find.

Key Takeaways from Q3 2021 – Toronto East Markets

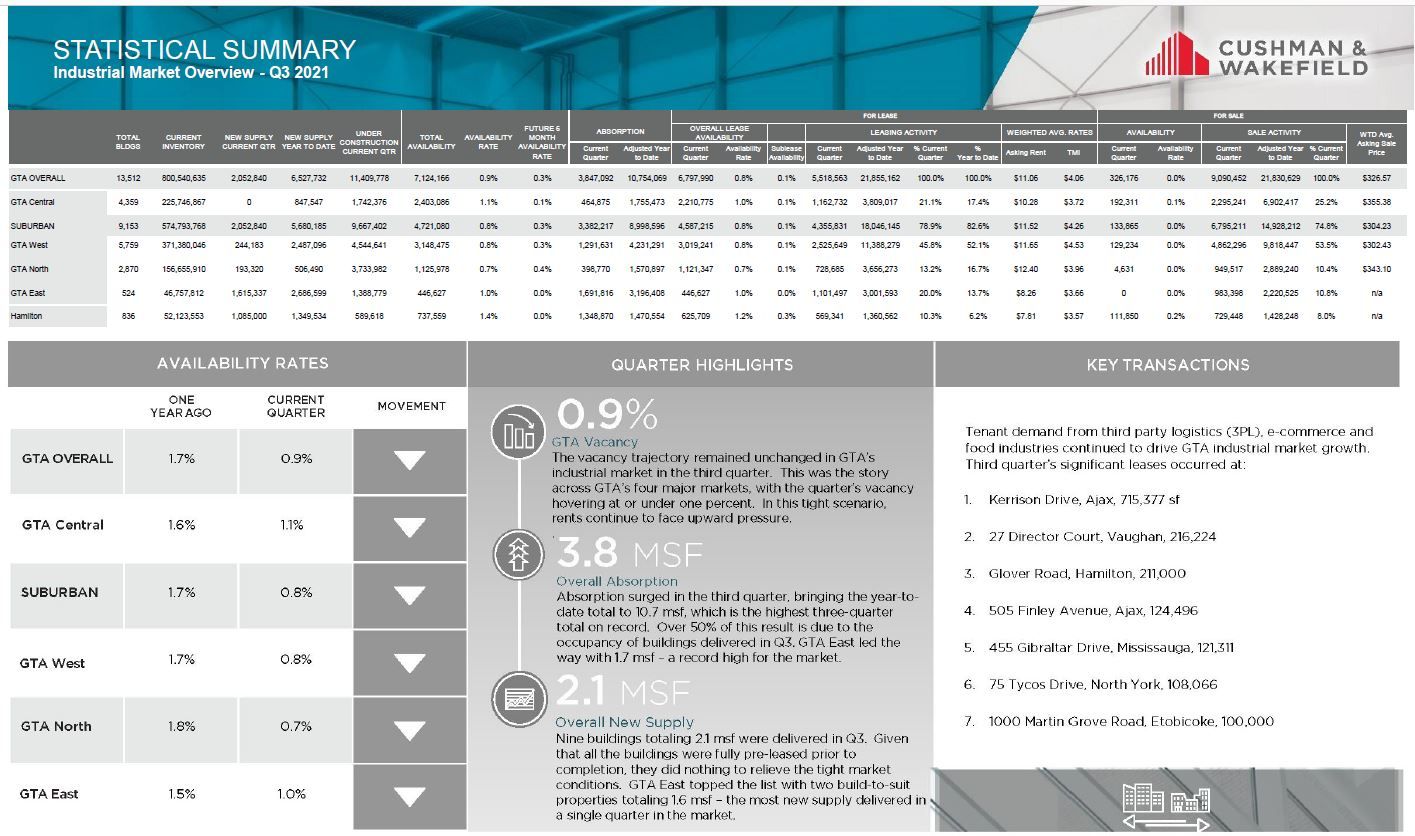

- The overall vacancy rate was 1.2% with 1.2% available for lease and 0% available for sale (no known on-market space for sale out of 46,757,812 SF of inventory);

- 1,615,337 SF of space was under construction;

- We had 1,615,337 SF of new supply; and there was

- No applicable weighted average asking sale price due to the non-existent inventory.

Why are the GTA East Markets in such demand?

Generally, the Toronto-East markets have strong economics – relatively inexpensive land compared to other markets in the GTA, better availability of land, better located industrial land with proximity to the City, relatively low development charges, and great access to major highways.

We have seen a number of major Users and Developers step in and make commitments on large pieces of land for spec development and design build, which amounts to millions of square feet being built and in the pipeline.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

This week we are covering the Toronto-East Markets (Pickering, Ajax, Whitby & Oshawa)

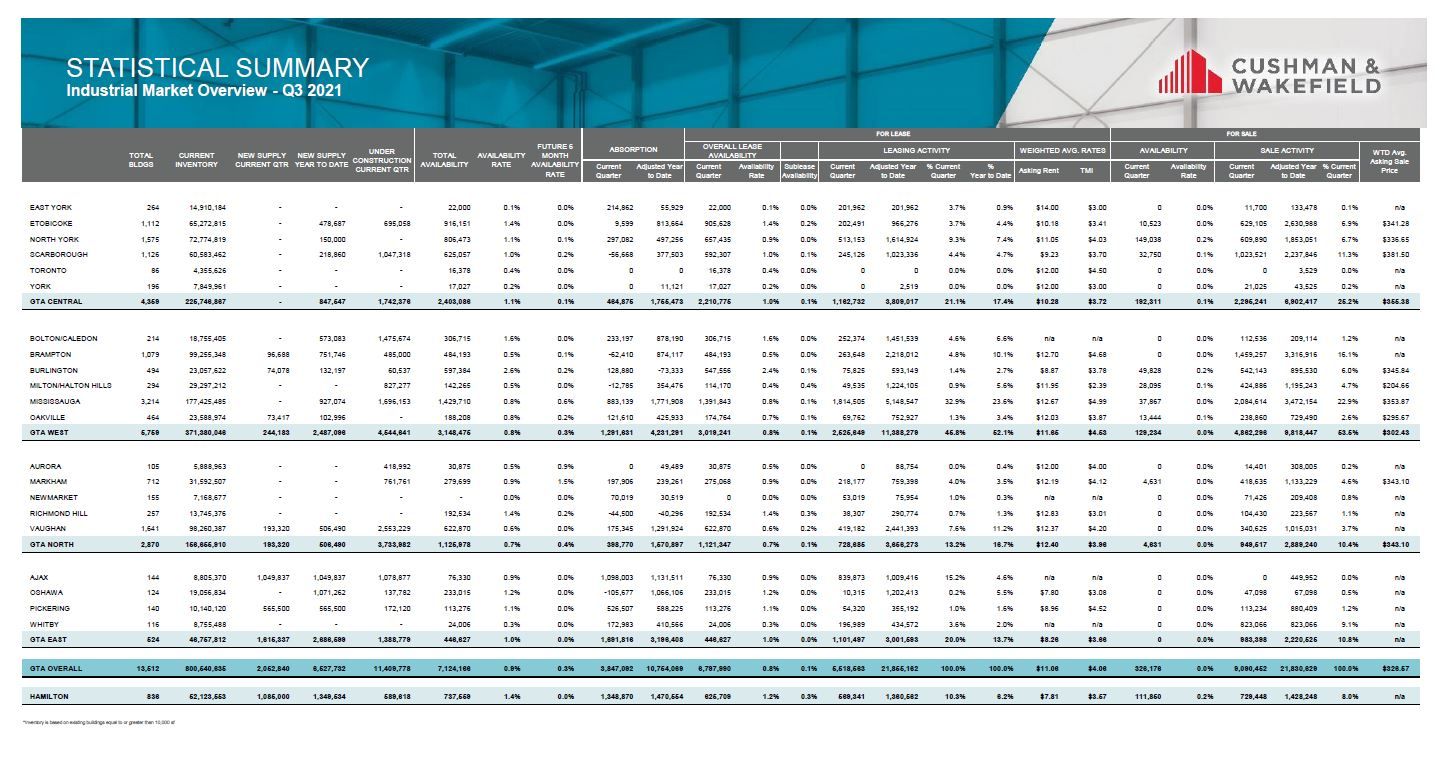

Statistical Summary – GTA East Markets – Q3 2021

Properties Sold between July 2021 – September 2021, from 20,000 SF plus

Properties Leased between July 2021 – September 2021, from 20,000 SF plus

GTA East Markets (Ajax)

Properties Sold between July 2021 – September 2021, from 20,000 SF plus

Properties Leased between July 2021 – September 2021, from 20,000 SF plus

Properties Sold between July 2021 – September 2021, from 20,000 SF plus

Properties Leased between July 2021 – September 2021, from 20,000 SF plus

2001 Forbes Street, Whitby

Properties Sold between July 2021 – September 2021, from 20,000 SF plus

Properties Leased between July 2021 – September 2021, from 20,000 SF plus

- Rental Rates: Currently, rental rates average $8.26 PSF in the GTA East, the lowest of all GTA submarkets; where all of the others are already in double-digits. We have already seen quite an increase in rental rates and land values in the East, with this trend poised to continue.

- Property Values: Property values, like rental rates, are considerably lower relative to the other GTA submarkets… but also increasing as investors and developers act on the opportunities and relative discount.

- Development Opportunities: We are seeing a lot more development than ever before. Big players such as Panattoni, Carttera, Crestpoint, Blackwood, PIRET, etc. (to name a few) are all involved… and it will continue.

Conclusion:

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation. And with our rental rates and valuations at all-time highs, and vacancy rates low, finding the right property is a real challenge.

Having said that, a lot of transactions are being done off the market.. and to participate in that, you should connect with experienced brokers that have long-standing relationships with property owners.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 29 years.

Goran Brelih is a Senior Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 29 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Senior Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com