April 4th, 2025

“There is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success than to take the lead in the introduction of a new order of things.”

- Niccolo Machiavelli

We are undoubtedly in an economic situation unseen for decades, if at all ever before.

The wave of new tariffs has left countless businesses – and governments – scrambling to formulate a response and to try to come up with a new, long-term strategy.

Most industries and, to go further, all aspects of our previous day-to-day lives will be impacted, whether directly or indirectly. We observe this to be true given the intricacies and interconnectedness of the global economy.

As such, the implications cover a vast array of topics and fields, but we will try to focus in on our narrow slice of expertise; industrial real estate within the Greater Toronto and Southern Ontario market. We will continue our exploration and analysis into the various facets but add in the latest tariff twists and how this may affect landlords, tenants, and investors.

Observation: anything can be overcome or achieved with a clear objective in mind.

By corollary: until we have certainty, making strategic decisions will be next to impossible.

As long as the ongoing ‘negotiations’ between global trade powers continues, and until we reach a new ‘equilibrium’ or ‘new normal’… no matter if it means re-shoring entire industries… businesses will be unable to make long-term commitments with respect to their manufacturing or distribution.

So for now, it appears that we are at a standstill for the broader market.

Local and regional players focused on kickstarting domestic production may take advantage of depressed demand to scoop up deals on leasing or purchasing assets. They may also benefit from any protectionist policies the Ontario or Canadian governments implement.

Companies with less complex or on-shored supply chains may also be better insulated from the fallout. Overall, well-positioned and risk-tolerant investors and occupiers may have select opportunities for the balance of 2025 to make a strategic play while others sit sidelined. That all said, until we know for sure how things will play out, it is going to be very difficult to convince others of that same vision.

We are watching the situation closely – as are most folks within the business world – and will continue to report on its impact to the GTA industrial real estate market. So without further ado, let’s switch back over to our analysis.

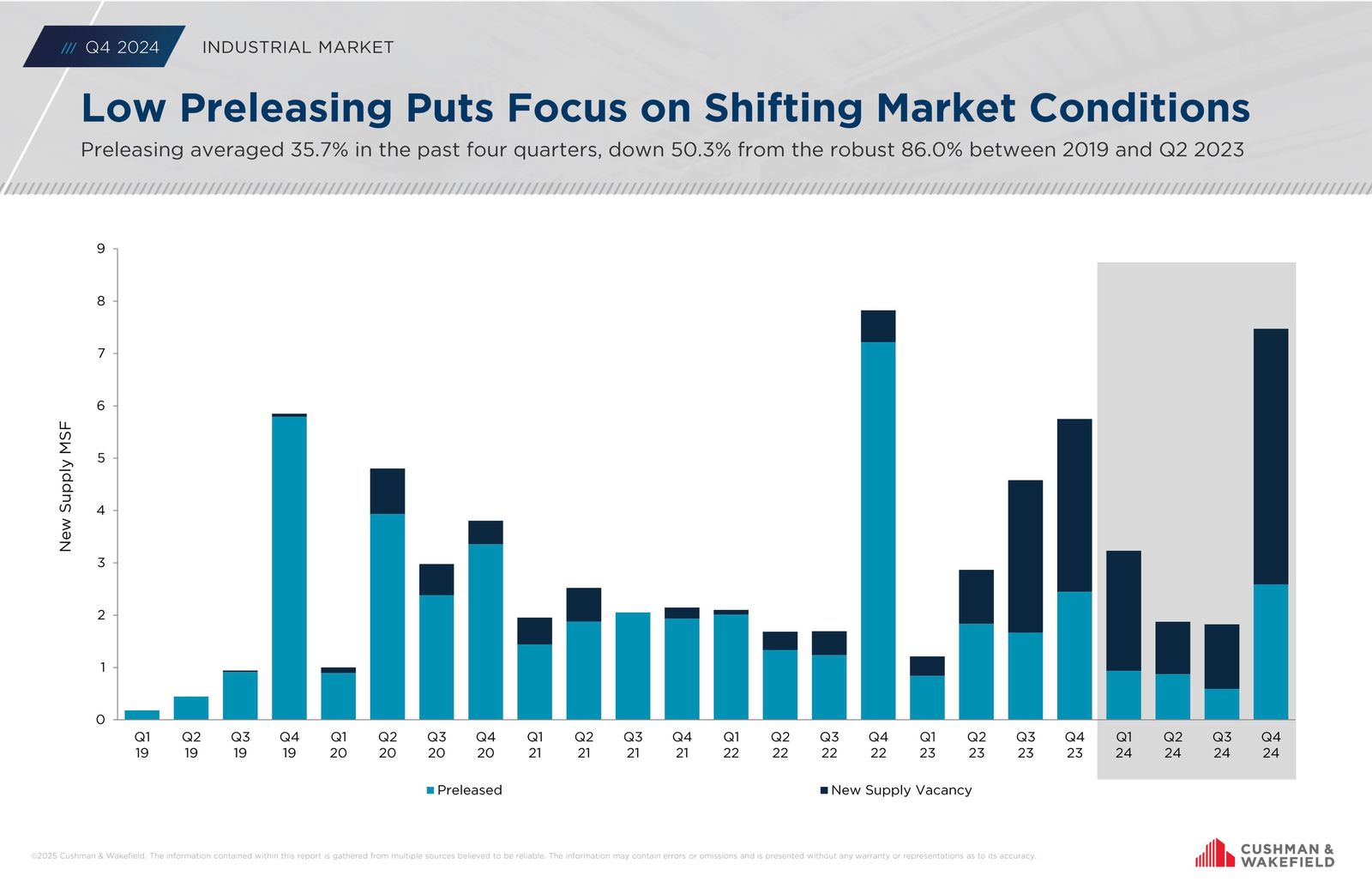

Market Context: The Pre-Leasing Plunge

Pre-leasing, the practice of securing industrial space leases before a building is completed, serves as a barometer for market confidence and demand. Historically, the GTA has seen robust pre-leasing, with rates reaching 86.0% between 2019 and Q2 2023, reflecting strong tenant interest and a tight market. However, recent data indicates a dramatic shift, with pre-leasing dropping to an average of 35.7% over the past four quarters—a 50.3% decline. This plunge underscores a market where developers are finding it increasingly difficult to lock in tenants early, pointing to an oversupply of space and a slowdown in demand.

The GTA industrial market has seen a record influx of new space, with 37.9 million square feet vacant as of Q4 2024, including 6.3 million square feet of sublease space. Demand, meanwhile, has hit an 11-year low, driven by economic headwinds such as rising interest rates, inflation, and shifts in industries like manufacturing and e-commerce. This supply-demand imbalance is a key factor behind the low pre-leasing rates, as tenants can afford to wait for better deals, reducing the urgency to commit early.

The Tariff Twist: Impact on Supply Chains and Distribution

Compounding this market shift are recent trade tariffs, particularly those imposed by the United States on Canadian goods, which are reshaping company strategies and, by extension, industrial real estate dynamics. On April 3, 2025, the US implemented an additional 25% tariff on all automobiles imported into the US, including passenger vehicles, light trucks, and certain auto parts, as reported by UPS Supply Chain Solutions. This tariff, effective from that date, targets Canadian exports, given Ontario’s significant role in North American auto production.

For GTA-based companies, especially in the automotive sector, these tariffs pose a direct threat.

Reduced competitiveness in the US market could lead to lower production volumes, as Canadian autos become more expensive for American consumers. This, in turn, may decrease the need for manufacturing and distribution space in the GTA, as companies scale back operations or delay expansions. The uncertainty surrounding trade policies further complicates matters, with businesses potentially postponing real estate decisions, contributing to the low pre-leasing rates.

Moreover, Canada’s retaliatory measures, imposing 25% tariffs on US goods starting March 13, 2025, as outlined by Canada.ca, add another layer of complexity. While these countermeasures aim to protect Canadian interests, they could increase costs for GTA companies sourcing US goods, potentially disrupting supply chains and affecting operational needs for industrial space.

However, there’s a countervailing force: tariffs on imports from other countries, such as China, could benefit Canadian manufacturers. For instance, a 20% tariff on Chinese-made goods, effective March 4, 2025, might make Canadian products more competitive in domestic and alternative export markets, potentially boosting demand for industrial space. Yet, given the specific impact on autos, the net effect for the GTA is likely negative, with reduced export opportunities weighing on space needs.

Stakeholder Implications: Navigating Uncertainty

The combination of low pre-leasing and tariff-induced uncertainty has distinct implications for market players:

- Developers face heightened risks, as building without secured tenants becomes more perilous. Submarkets like GTA East, with vacancy rates at a 10-year high due to record new supply, exemplify this challenge. Developers may need to focus on high-quality projects in prime locations or offer flexible terms to attract tenants, mitigating the risk of speculative inventory.

- Tenants gain leverage in negotiations, with increased availability allowing them to delay decisions or secure better rates. This is particularly true in oversupplied segments, where tenants can push for lower rents, shorter terms, or incentives like tenant improvement allowances. However, they must balance this with the potential for supply chain disruptions due to tariffs, which could affect long-term space needs.

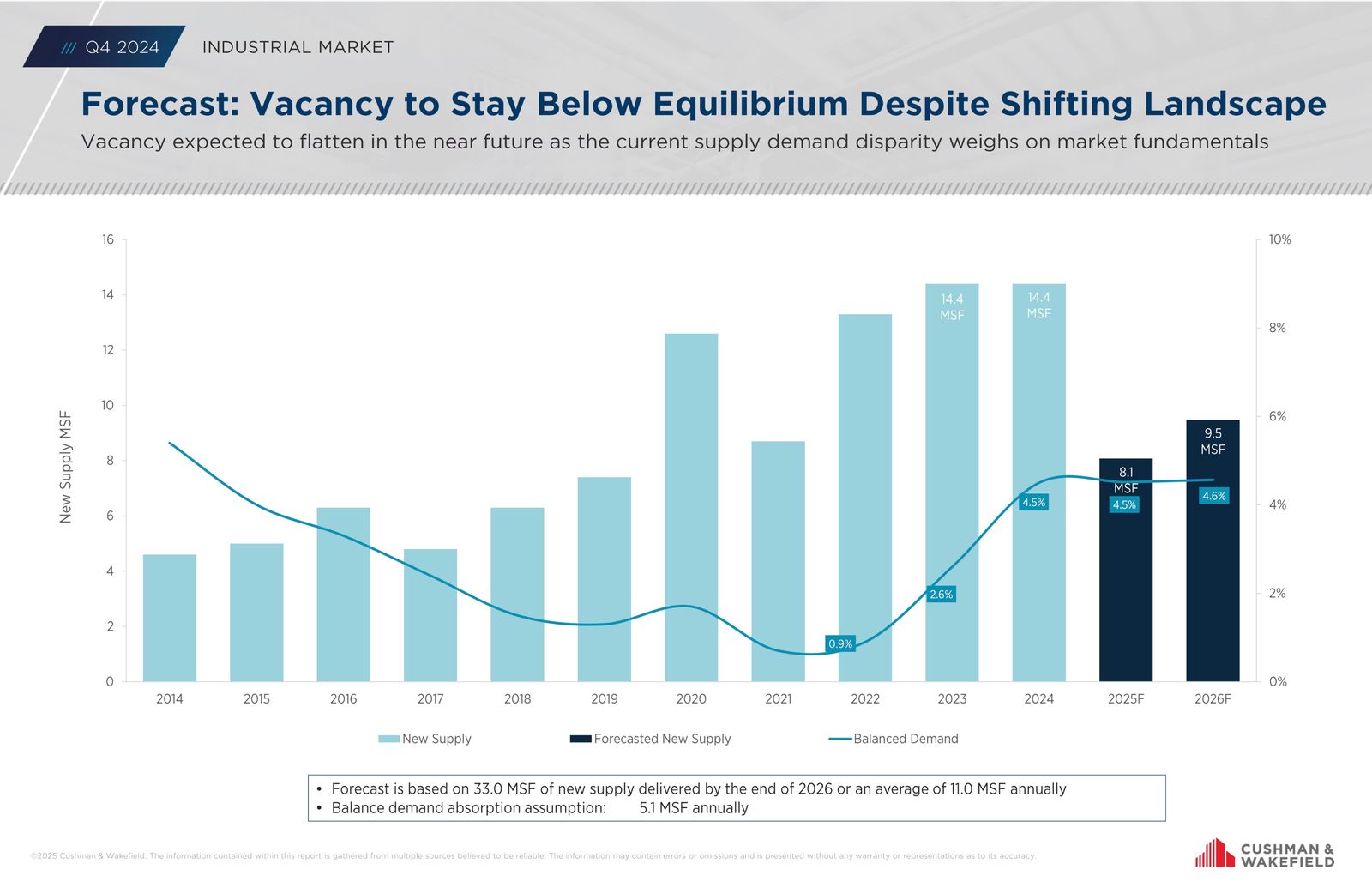

- Investors must tread carefully, assessing risks and opportunities. The softening market, exacerbated by tariffs, may present distressed assets at lower prices, but investors should prioritize properties with strong fundamentals—modern facilities in strategic locations—to weather short-term turbulence. The GTA’s role as a logistics hub, with 33.0 million square feet of new supply projected by 2026, suggests long-term potential, but tariff impacts could delay recovery.

Future Outlook: A Market in Transition

Looking ahead, the GTA industrial market is likely to see a period of adjustment. Forecasts suggest vacancy rates may plateau below equilibrium by 2026, with demand absorbing roughly 5.1 million square feet annually.

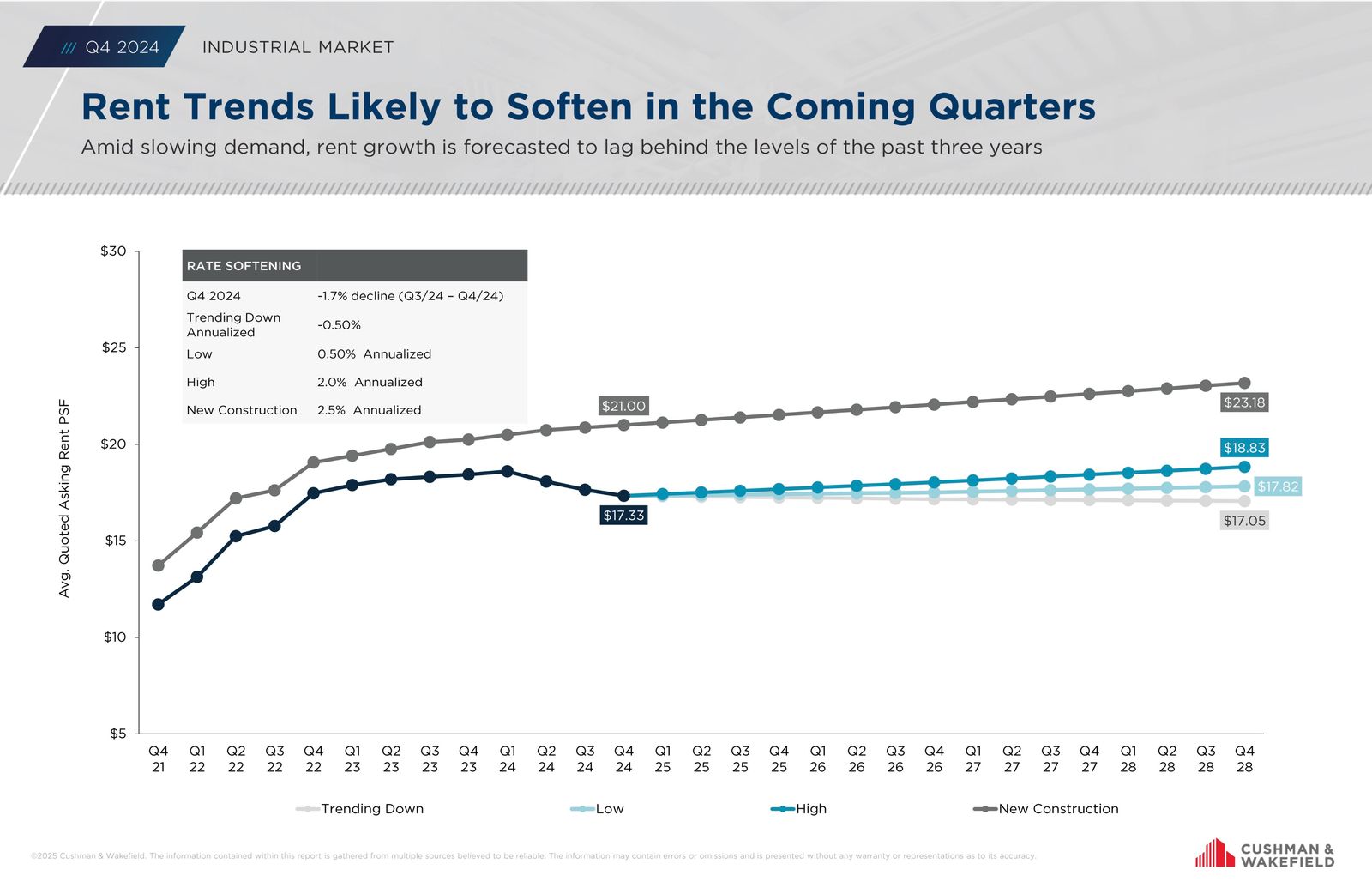

However, tariff-related uncertainties could prolong this transition, with companies potentially re-shoring operations or consolidating space, affecting pre-leasing rates further. The market’s average lease rate of $17.33 per square foot, still among North America’s top tier, provides a foundation for resilience, but stakeholders must remain agile.

Strategic Takeaways

- Landlords: Flexibility—through competitive pricing, shorter lease terms, or enhanced tenant incentives like rent abatement—will be key to filling vacant spaces in a market clouded by tariff-induced uncertainty. With tenants hesitant to commit long-term due to shifting supply chains, landlords should emphasize adaptable lease structures or showcase a property’s versatility (e.g., its ability to serve multiple industries). This is especially vital in oversupplied areas like GTA East, where vacancy rates have hit a 10-year high.

- Tenants: Now’s the time to negotiate favorable leases, especially in oversupplied submarkets like GTA East, where low preleasing rates give tenants an edge. Take advantage of the uncertainty—fueled by both oversupply and tariffs—to secure lower rates, flexible terms, or extras like tenant improvement allowances. At the same time, consider how trade disruptions might impact your supply chain and space requirements to ensure your lease aligns with operational needs.

- Investors: Focus on properties with strong fundamentals and long-term growth potential to weather short-term turbulence from low pre-leasing and tariff-related risks. Prioritize assets in prime locations or those tied to industries less affected by trade disruptions, such as e-commerce or local manufacturing. Properties with diversified tenant bases and modern infrastructure near logistics hubs offer resilience and promise sustained value despite market fluctuations.

Conclusion:

The GTA industrial market faces challenges like low preleasing rates and tariff uncertainties, yet opportunities abound for those who adapt. Landlords can offer flexible terms, tenants can negotiate better deals, and investors can focus on resilient assets. Success in this shifting landscape will depend on agility and strategic foresight.

In the meantime, for a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih<

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com