As 2025 unfolds, the industrial real estate sector stands at a pivotal moment.

The Cushman & Wakefield “Midpoint 2025 Economic and CRE Outlook” paints a picture of resilience amid tariff-driven volatility and economic uncertainty.

With capital markets showing signs of recovery and industrial assets remaining a cornerstone of investment portfolios, opportunities abound for savvy investors and occupiers.

For today’s issue, we’ll dive into the evolving capital market landscape and strategic moves to thrive in this dynamic environment. From stabilizing valuations to leveraging supply constraints, we’ll uncover how stakeholders can position themselves for success in the industrial market.

Although the report is centered around the American economic landscape, historically, these trends have largely followed north of the border. Whether or not that continues, this data can provide another perspective for where the Toronto industrial market may be headed in the coming months and years.

So without further ado, let’s continue our discussion from our previous newsletter and look at the capital markets as well as strategic opportunities industrial real estate.

Section 1: Capital Markets: A Turning Point

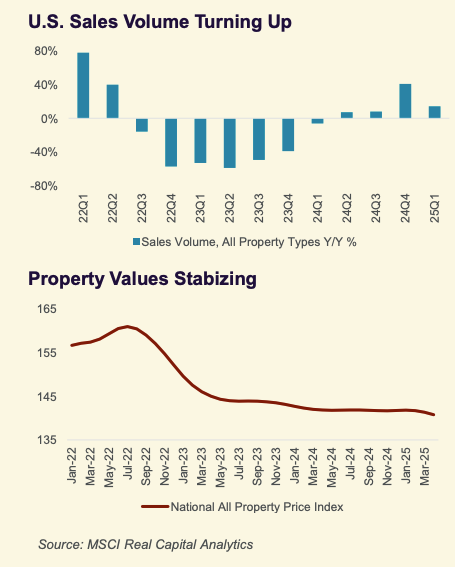

The capital markets for commercial real estate are showing tentative signs of recovery, with industrial assets remaining a favoured investment class. Cushman & Wakefield reports a 15% year-over-year increase in CRE transaction volumes in Q1 2025, driven by institutional capital and portfolio deals. Industrial properties, with their durable income streams, are particularly attractive amid economic uncertainty. The report notes that net operating income (NOI) growth is expected to pick up modestly in 2025, supported by stabilizing fundamentals and diminishing supply pipelines.

US Capital Markets Forecast – Source: Cushman & Wakefield Research.

However, base rate uncertainty persists. The Federal Reserve is expected to cut rates twice in 2025, with the fed funds rate dropping to 3.75% by year-end, but market participants are equally split on whether fewer or more cuts will occur. The 10-year Treasury yield is projected to hover between 4.0-4.5%, consistent with long-run equilibrium. Despite this volatility, debt costs have declined 35-50 basis points from 2023 peaks, and lender diversity is increasing, with debt funds, CMBS, and banks becoming more active. For industrial investors, this means improved financing availability, particularly for high-quality assets in prime logistics hubs.

Cap rate expansion is creating favorable buying conditions, with valuations stabilizing as NOI growth strengthens. The report emphasizes that CRE, including industrial, benefits from its status as a real asset during inflationary periods. Investors should seize opportunities to acquire assets from motivated sellers, particularly in markets with limited new supply. The “higher-for-longer” interest rate environment is here to stay, but the report suggests that capital markets are adjusting, with transaction volumes and pricing expected to rise incrementally over the next 12 months.

Section 2: Strategic Opportunities for Investors and Occupiers

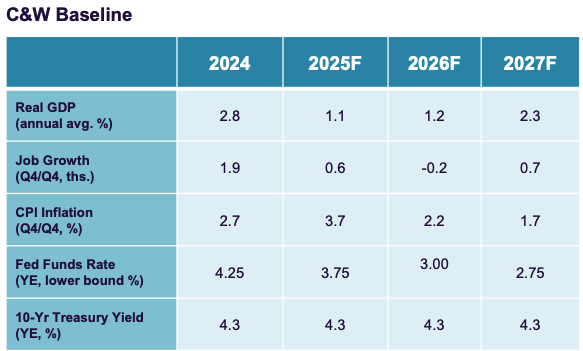

For investors, the industrial sector offers a compelling long-term thesis. The Cushman & Wakefield report highlights secular themes—such as e-commerce, nearshoring, and manufacturing—that underpin industrial demand. With new construction slowing (186.4 msf in 2026 vs. 430.0 msf in 2024), markets with constrained supply are primed for occupancy and rent growth in 2026-27. Investors should target well-located assets in high-demand corridors, such as ports and inland distribution hubs, where tariff impacts are less pronounced.

US Economic Forecast – Source: Cushman & Wakefield Research.

Occupiers face a different set of challenges and opportunities. The report advises maintaining a long-term perspective, using the current uncertainty to negotiate favorable lease terms. With rent growth projected to remain flat or negative through 2026, occupiers can lock in cost-effective spaces, particularly in markets with rising vacancies. The report also recommends diversifying supply chains to mitigate tariff risks, leveraging 3PLs to enhance operational flexibility. Large corporations are poised to gain market share post-uncertainty, and proactive occupiers can position themselves for growth by securing high-quality assets now.

Both investors and occupiers should reassess their risk profiles. The report’s baseline scenario assumes a soft landing, with GDP growth slowing to 1.1% in 2025 before rebounding to 2.3% in 2027. However, downside scenarios, including a mild recession (25% probability) or stagflation (10% probability), highlight the need for contingency planning. Focusing on necessity-based assets—such as warehouses serving essential goods—can provide stability in weaker growth environments.

Conclusion:

The industrial real estate market in 2025 offers a mix of challenges and opportunities. Capital markets are stabilizing, and strategic investors can capitalize on favourable buying conditions, while occupiers can leverage softer rents and uncertainty to optimize their portfolios. By focusing on long-term fundamentals and high-quality assets, stakeholders can navigate the current volatility and position themselves for a rebound in 2026.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com