May 9th, 2025

Another week has gone by and investors and occupiers alike remain uncertain about how the economic landscape will unfold in the coming weeks and months.

A looming federal election, along with tense international events are permeating into stakeholder expectations; which, if you’re a student of economics you may realize is often a greater contributor to outcomes than the underlying fundamentals themselves.

In any event, we notice and see market players making moves to hedge short-term risks with respect to their industrial assets. As a whole, the sentiment seems to be that we are potentially going to see some near-term volatility; with optimists hoping for a regenerative period in the latter half of 2025 going into the new year.

As such, Tenants are looking for low-cost options to bridge any gaps in their footprint needs, while also looking to mitigate rent increases or consolidate their operations where possible. Sublease opportunities, whether on- or off-market are out there – and we notice businesses making quick, short-term deals to optimize their space for the balance of the year.

Likewise, Investors are doing their best to quickly lease-up vacant space with significant discounts and incentives – which they are willing to stomach until we get to the other side of this uncertain period.

For those Parties well-positioned to acquire assets, there may not have been a better time to do so in the last 5-10 years. Prices have fallen and, following the softer market in 2023 and 2024, owners are now more amenable to the fact that values are not where they were following the post-lockdown boom.

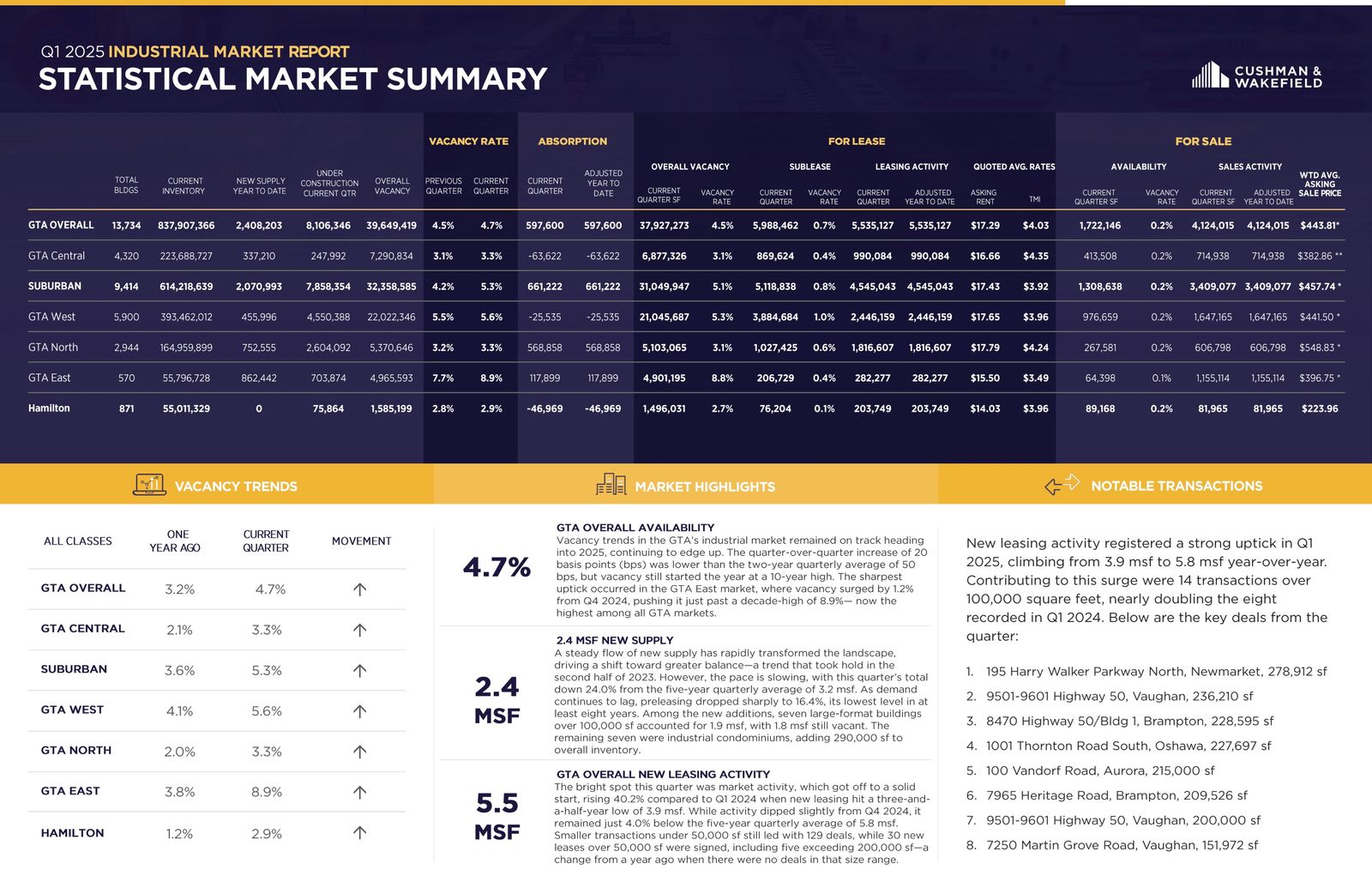

The GTA West markets of Mississauga, Brampton, Milton, Halton Hills, Oakville, Burlington, and Caledon are sought-after for their access to labour, transportation routes, dense populations, strategic access to the Toronto core, US border, and southwestern Ontario economic base. They themselves also contain several of Canada’s largest cities (Mississauga and Brampton) and with proximity to Toronto Pearson International airport, the Port of Hamilton, and several intermodal yards, the GTA West is definitively the industrial epicentre of the GTA – and of Canada.

So without further ado, let’s examine how the Greater Toronto Area West submarkets performed in Q1 2025, and where we expect the market to go moving forward.

- The availability rate increased from 5.5% to 5.6%, with 5.3% available for lease and 0.2% available for sale;

- We had 455,996 SF of new supply year-to-date and 4,550,388 SF still under construction;

- We had 25,535 SF of negative absorption;

- Brampton achieved the highest weighted asking net rental rates in Q1 2025 at $17.90 PSF, followed by Mississauga and Milton/Halton Hills both at $17.68 PSF;

- The weighted average asking net rent was $17.65 PSF, down from $17.71 the previous quarter, with additional rent of $3.96 PSF (an increase from $3.89 PSF); and

- The weighted average asking sale price fell from $448.46 PSF to $441.50 PSF; with values largely determined by industrial condo sales.

Why are the GTA West Markets in such demand?

The GTA West Industrial Markets are by far the largest industrial markets in the GTA, representing about 47% of GTA Industrial Inventory, or 393,462,012 SF. The GTA West Markets were active this quarter and with more than 4,550,388 SF under construction.

So, if you are an Investor, Landlord, or Owner-Occupier you may be wondering…

“How much is my property really worth?”

What rental rate can I expect? How much $/PSF would I be able to get if I sold my building?

These questions are being asked all the time.

The answer to this will depend on a range of factors, including:

- the age and size of the building,

- lot size,

- ceiling height,

- office component,

- parking,

- trucking access,

- truck parking if available, etc….

This week we are covering the Toronto-West Markets

(Mississauga, Brampton, Oakville, Milton, Caledon, Burlington & Halton Hills)

Statistical Summary – GTA West Markets – Q1 2025

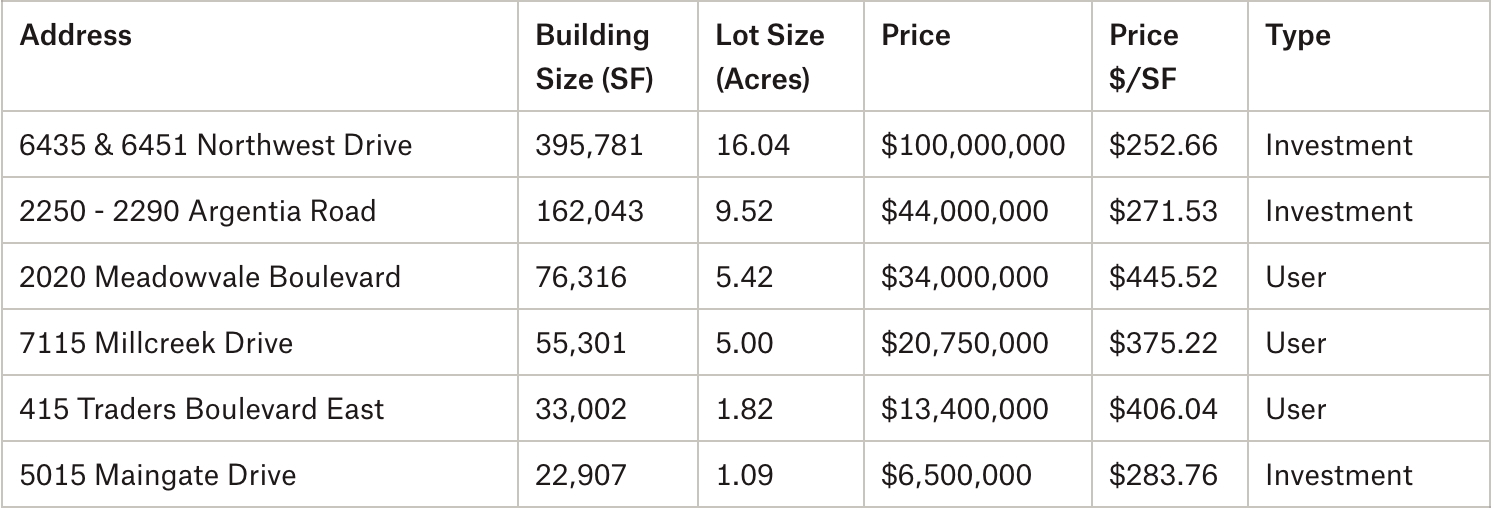

Properties Sold between January 2025 – March 2025, from 20,000 SF plus

6435 & 6451 Northwest Drive, Mississauga.

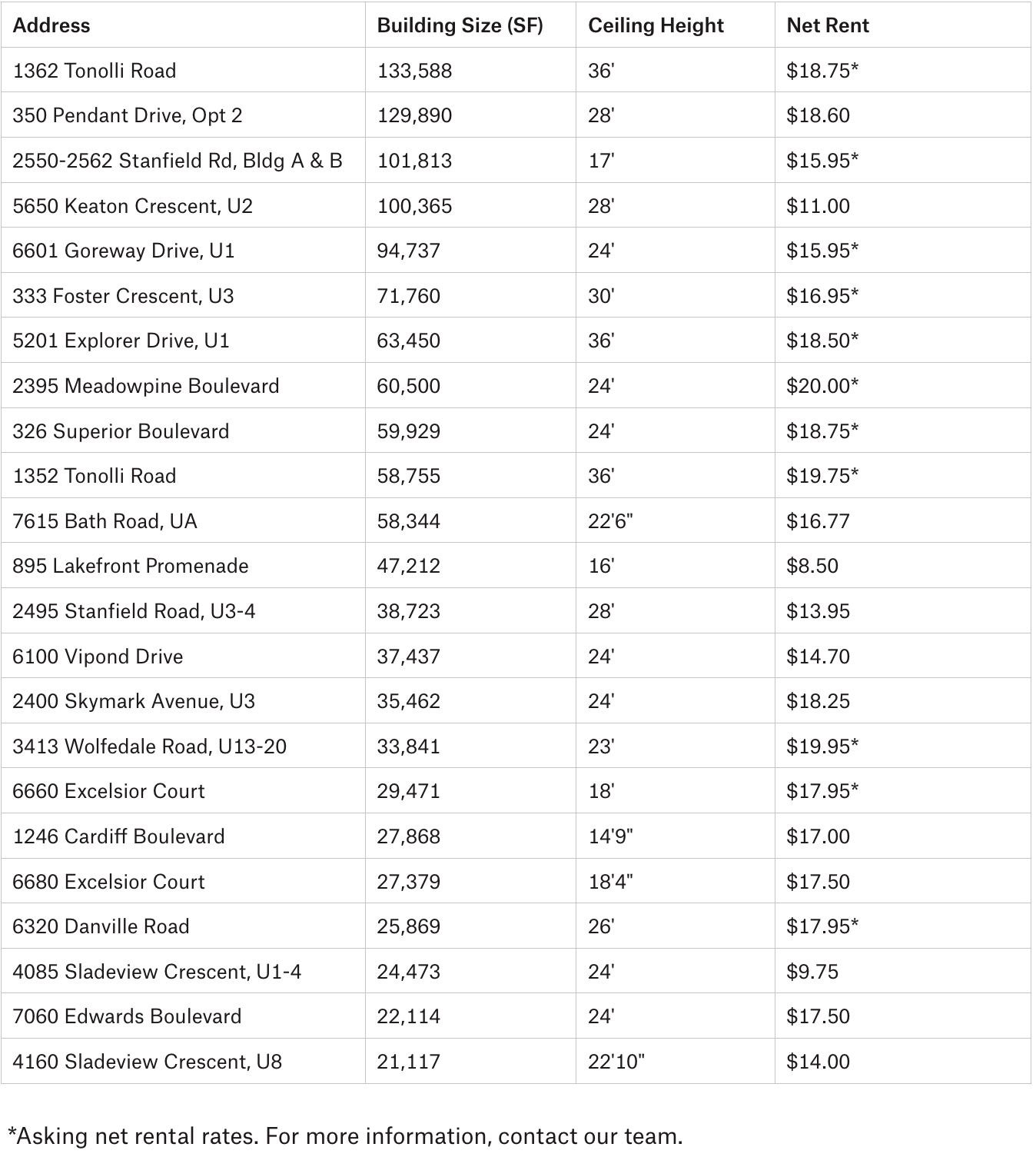

Properties Leased between January 2025 – March 2025, from 20,000 SF plus

1362 Tonolli Road, Mississauga.

7900 Airport Road, Brampton.

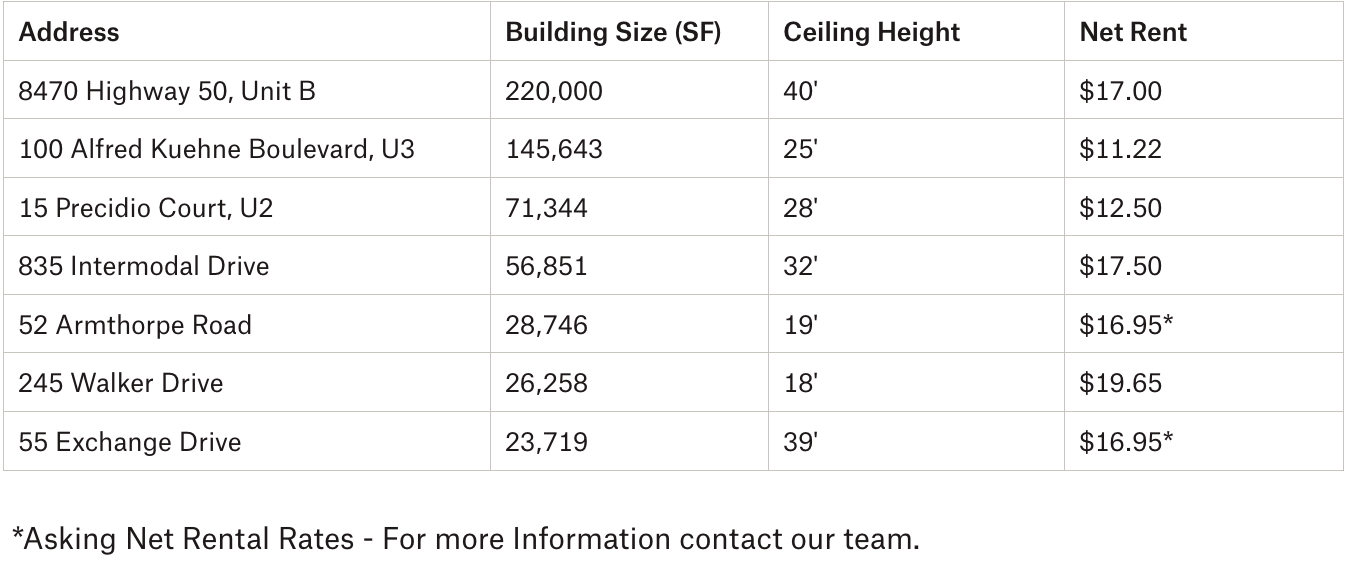

Properties Leased between January 2025 – March 2025, from 20,000 SF plus

8470 Highway 50, Brampton.

2700 Bristol Circle, Oakville.

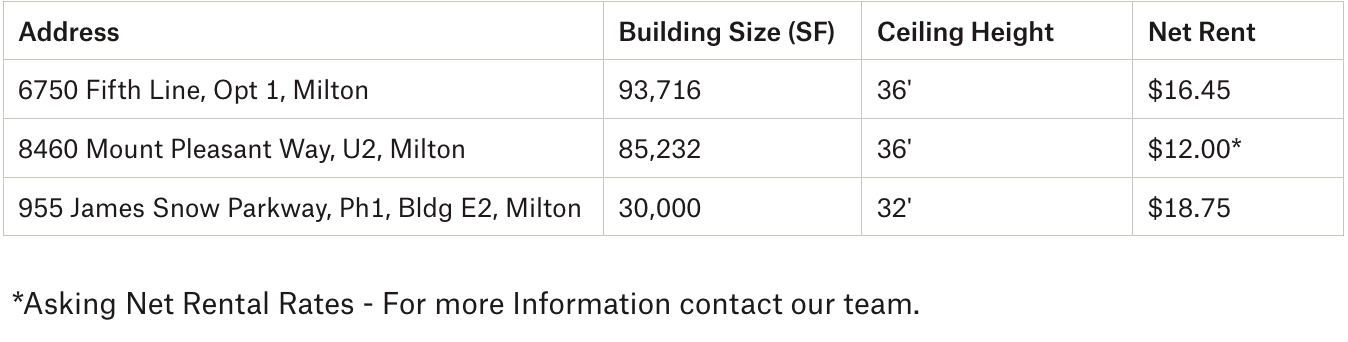

Properties Leased between January 2025 – March 2025, from 20,000 SF plus

6750 Fifth Line, Milton.

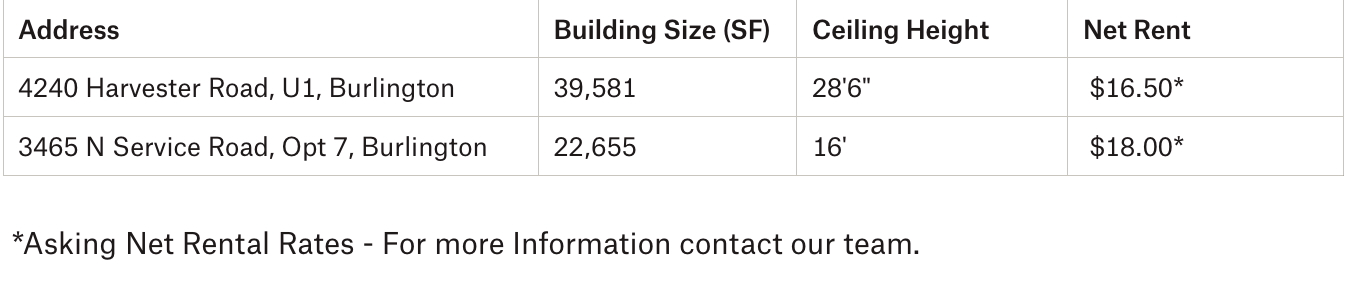

4240 Harvester Road, Burlington.

- Rental Rates: Rents continue to adjust and, in many cases, we continue to see rate reductions. We expect this to continue. Likewise, annual rental escalations have plateaued and have decreased. Leasing is picking up and businesses are making decisions, however, the ongoing threat of tariffs are a concern. Further, there is continued downward pressure on rents, specifically in Class B or C industrial buildings. Overall, we are in a more balanced market between Landlords and Tenants.

- Property Values: As rental rates plateau, and as we see rents decrease in certain properties, we are going to see a decrease in value of investment properties. The recent and continued interest rate cuts may stabilize this trend, however. For users, we expect to see values remain elevated as supply of properties for sale is extremely limited. Finally, and despite the downward trend of interest rates, previously elevated levels have decreased the value of development land.

- Development Opportunities: In the first quarter of 2025, we had approximately 4.55 million square feet under construction in the GTA-West markets. This represents about 56% of all new development across the GTA (8.1 million SF), with the bulk of activity taking place in Mississauga (1.54 MSF) and Brampton (1.24 MSF).

Conclusion:

So, how much is your property really worth?

What rental rate can you expect or how much per SF would you be able to get if you sell your building? How much can we compress CAP rates to create even greater value?

Well, the answers to these questions will depend on a variety of factors, many of which we can quickly uncover in an assessment of your situation. And with our rental rates and valuations at all-time highs, and vacancy rates low, finding the right property is a real challenge.

Having said that, a lot of transactions are being done off the market.. and to participate in that, you should connect with experienced brokers that have long-standing relationships with property owners.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com