March 14th, 2025

What happens when a market that’s been running hot for a decade suddenly cools? In the GTA’s industrial sector, the answer is unfolding now: rental rates are easing across the board, with a 1.2% drop in the past quarter alone—the third consecutive decline after years of relentless growth. For landlords, tenants, and investors alike, this isn’t just a statistic—it’s a signal.

Following Part 1’s deep dive into the supply-demand pivot reshaping the GTA’s industrial landscape, Part 2 turns the lens on rental trends and what lies ahead.

From the softening rates hitting small-bay properties to the cautious optimism for a 2025 recovery, we’re breaking down the data and uncovering the opportunities in this shifting market.

Read on to understand what’s driving this change—and how to position yourself for what’s next.

Softening Rents and Shifting Conditions: What’s Next for the GTA?

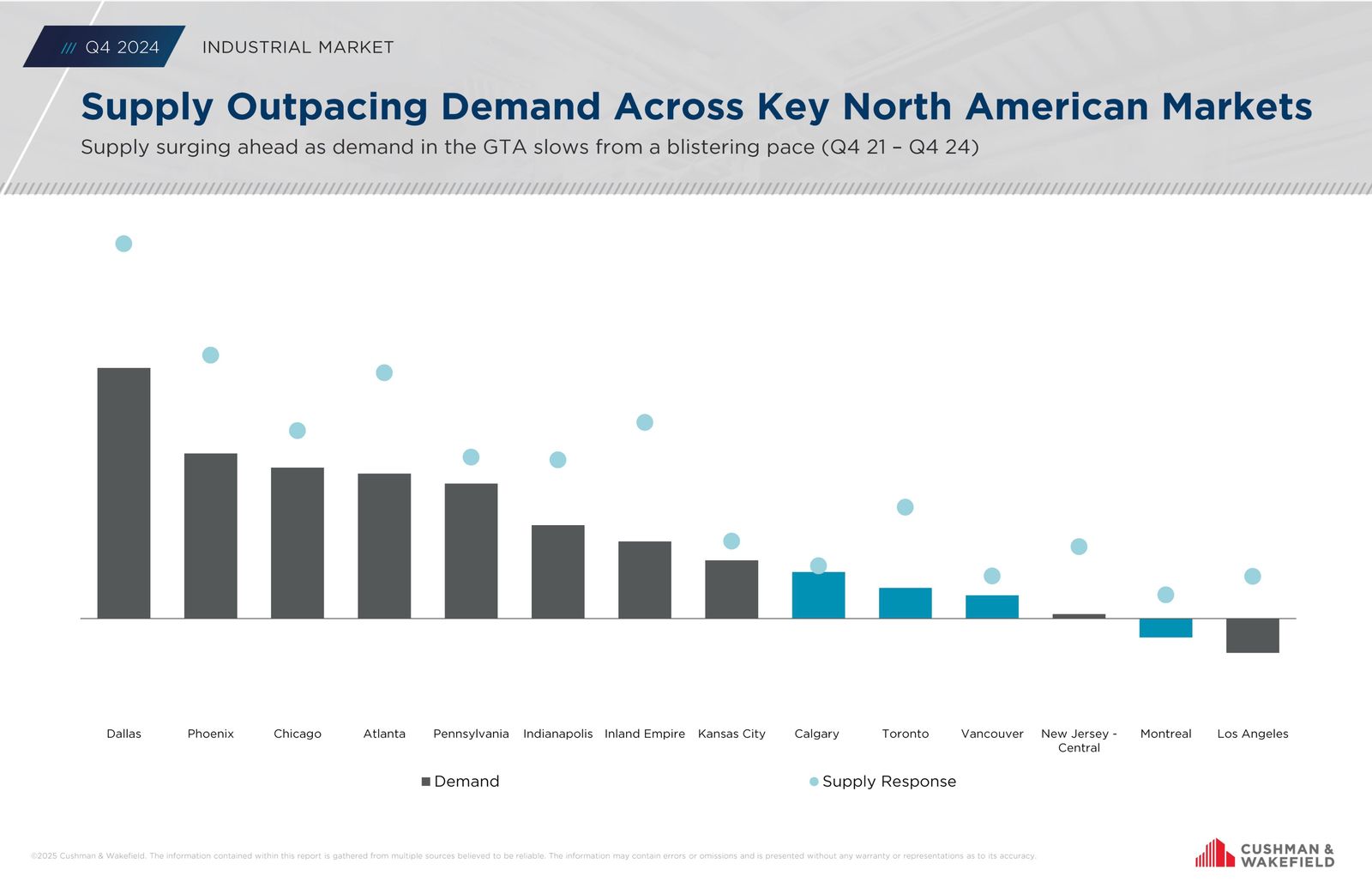

Two weeks ago, we examined the GTA’s industrial market, where a surge in supply and a dip in demand have driven vacancy rates to a nine-year high. Now, we turn to the ripple effects on rental rates and the forecast ahead. As rental growth slows and pre-leasing falters, what can stakeholders expect in the coming quarters?

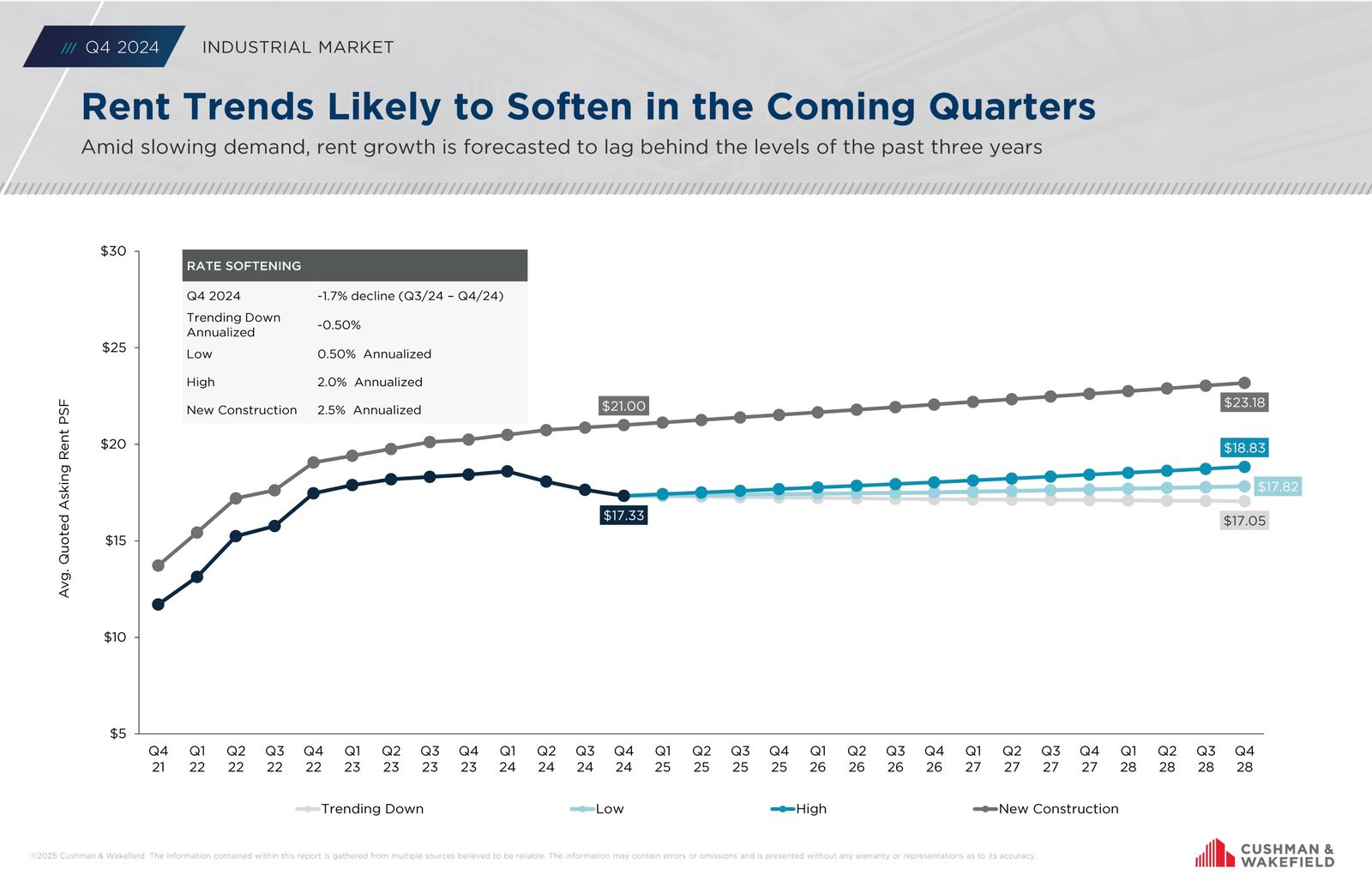

Rental Rates: A Leader Losing Momentum

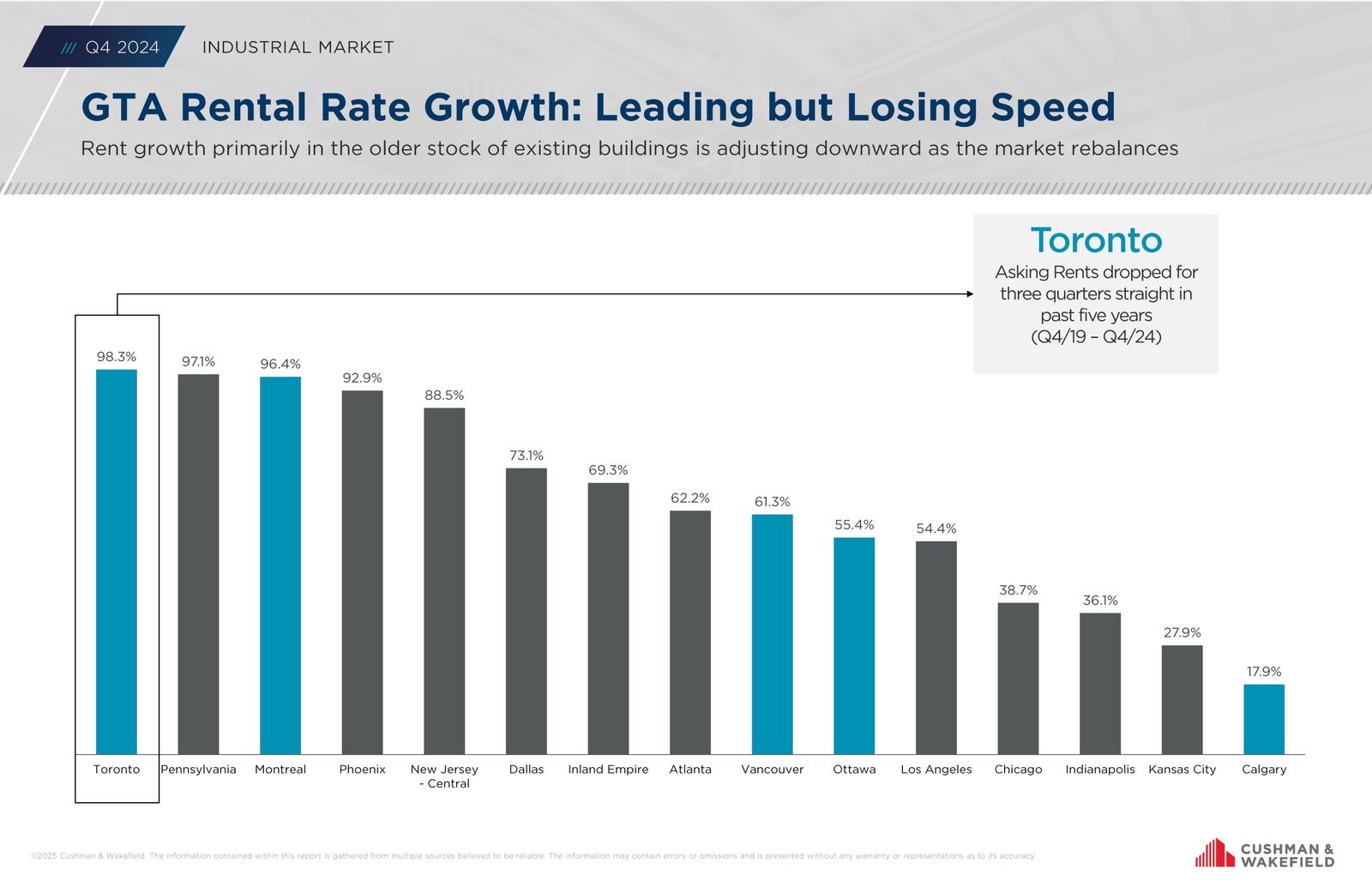

The GTA has long been a frontrunner in industrial rental rate growth, fueled by tight supply and soaring demand in recent years. However, the tide is turning. Cushman & Wakefield’s Q4 2024 report notes that asking rents have dropped for three consecutive quarters—the first such streak in five years (Q4 2019–Q4 2024).

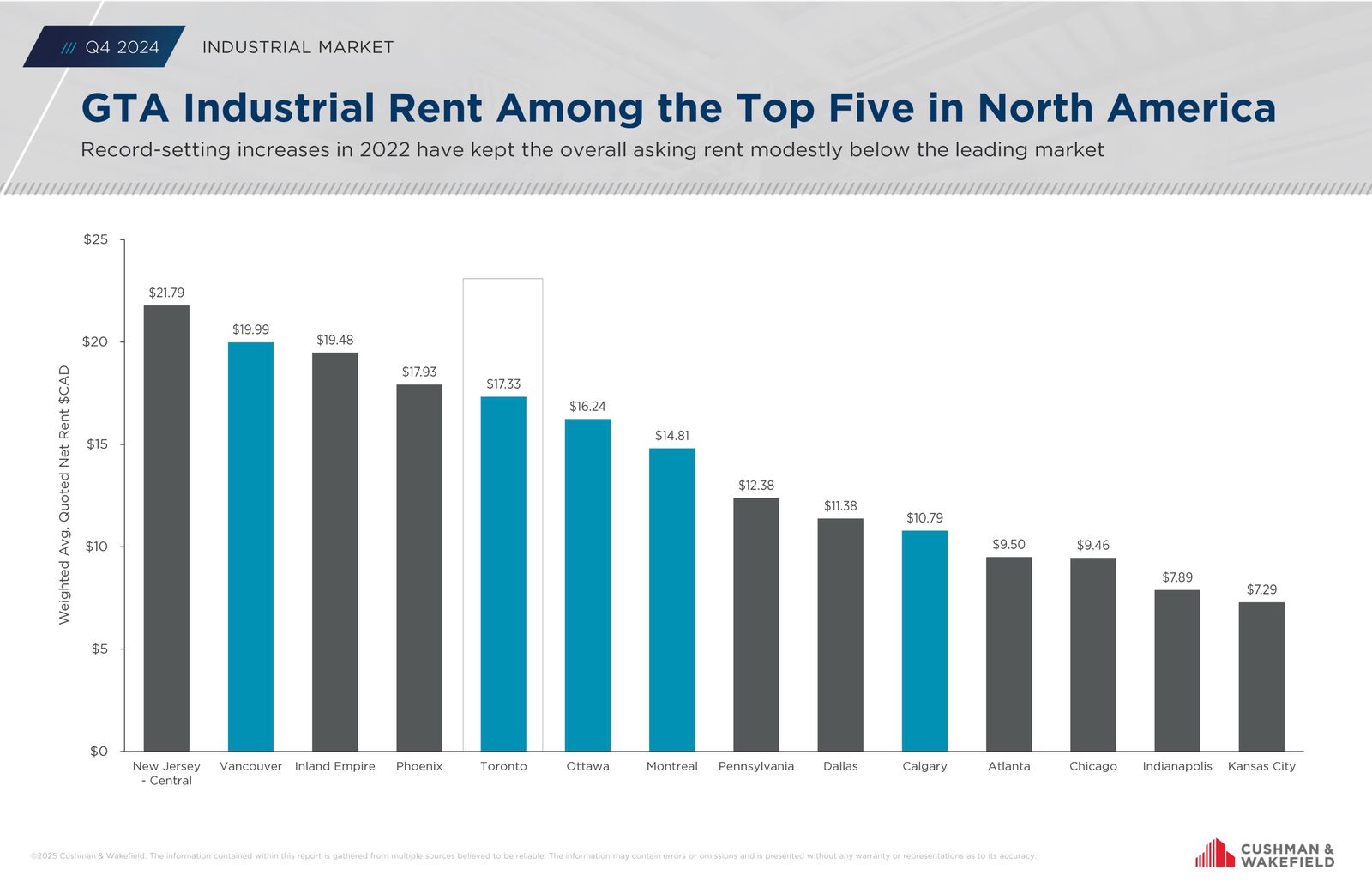

Toronto’s average asking rent stands at $17.33 per square foot, placing it among North America’s top five markets but below leaders like Vancouver ($25) and Inland Empire ($17.93). This softening reflects the market’s rebalancing as vacancy climbs.

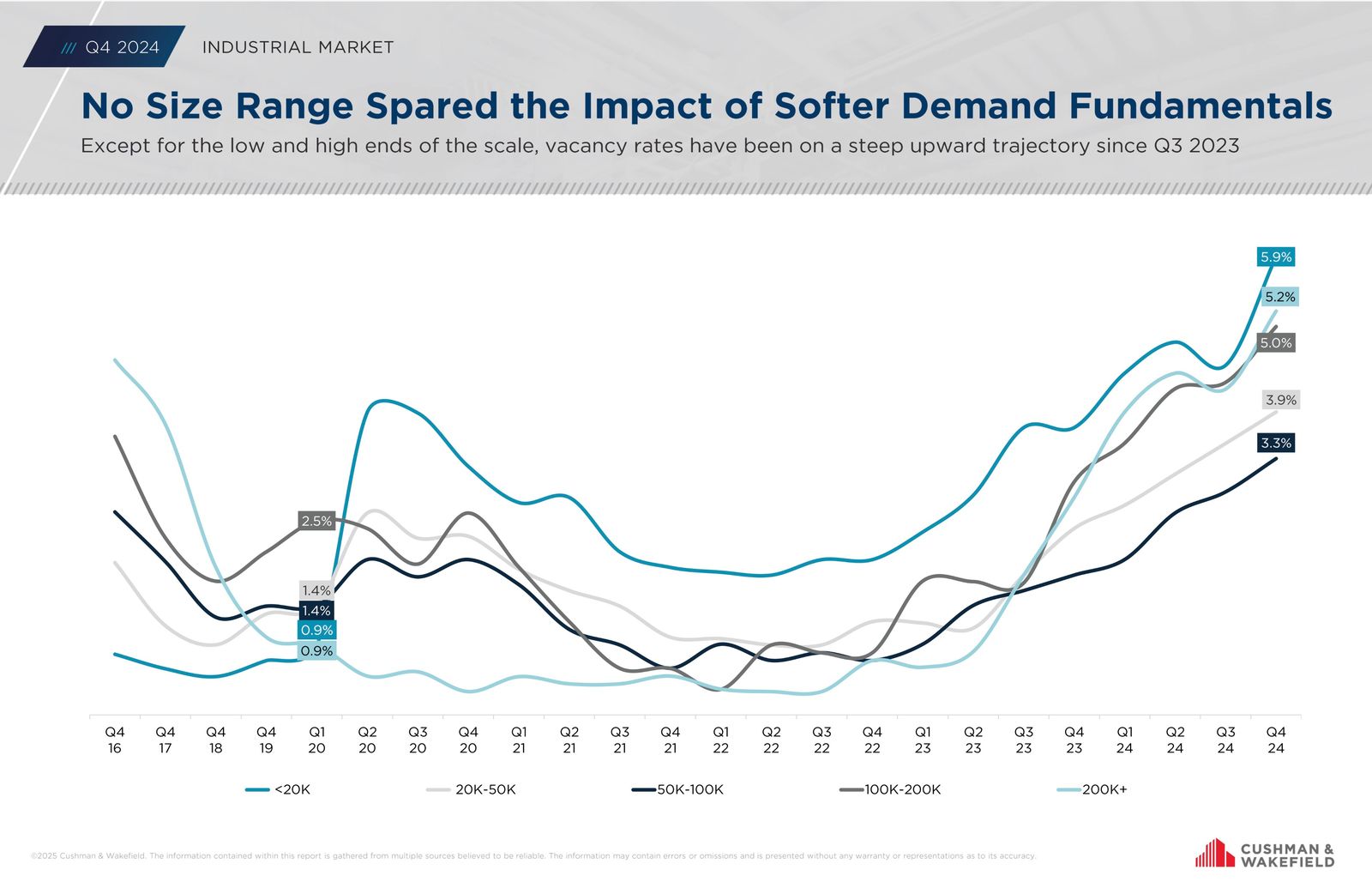

Pressure Across Size Ranges

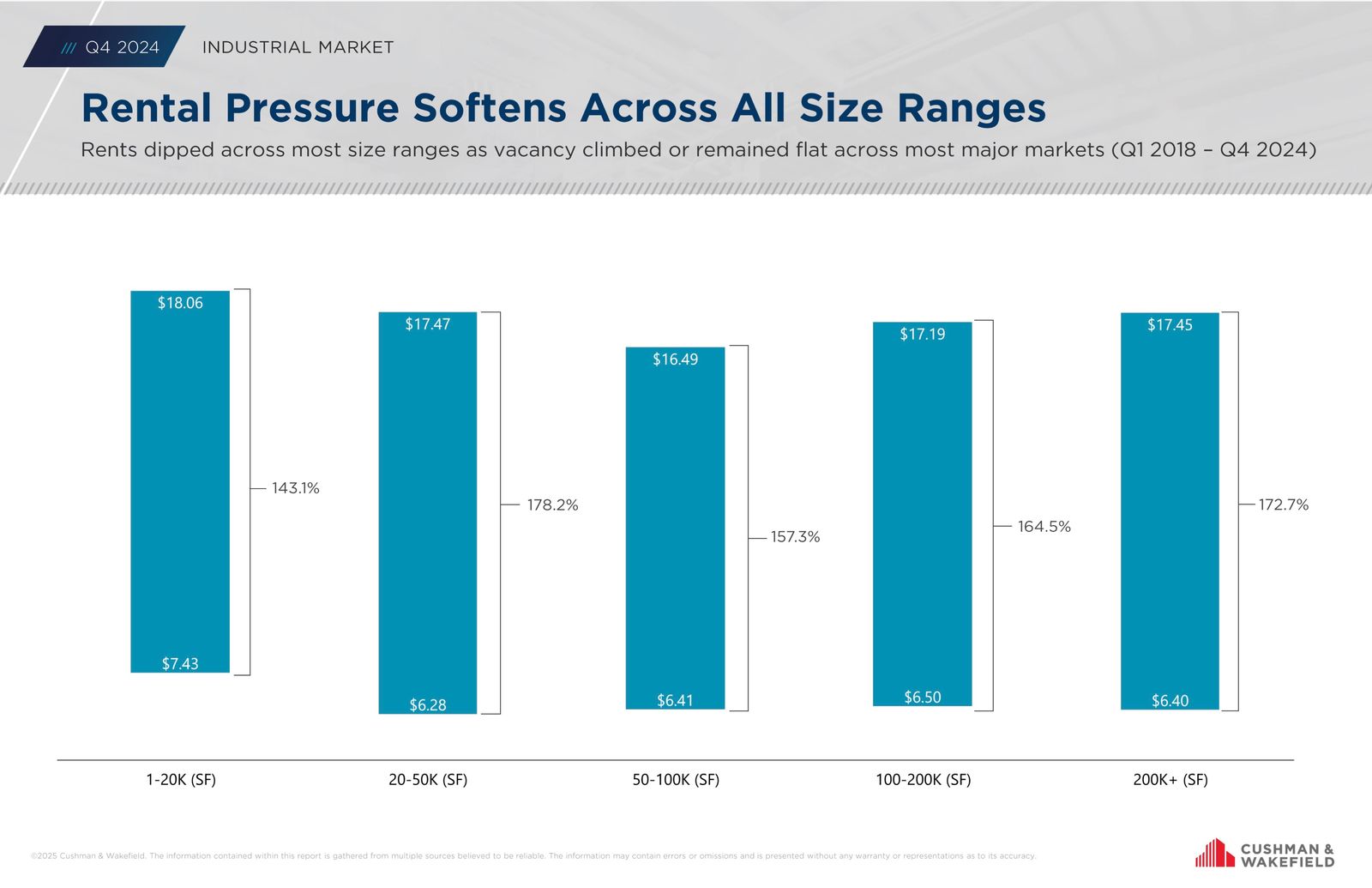

The rental dip isn’t uniform. Rents have softened across most size ranges—from small spaces (1-20K SF) to large facilities (200K+ SF)—as vacancy either rises or stagnates. This trend, observed from Q1 2018 to Q4 2024, signals that tenants across industries are benefiting from increased options, diluting the pricing power landlords enjoyed during the market’s peak. Older building stock, in particular, is seeing downward adjustments as newer, high-spec properties dominate leasing activity.

No size range is immune to the GTA’s rising vacancy rates, which have surged since Q3 2023. By Q4 2024, smaller spaces under 20,000 square feet hit 3.3% vacancy, while larger properties over 200,000 square feet reached 5.9%. This broad uptick reflects softer demand, likely pushing rental rates downward as landlords compete to fill spaces. Tenants, this is your moment—especially in larger properties—to negotiate better deals. Landlords may need to get creative with pricing or perks to keep occupancy strong as the market adjusts.

Preleasing Woes: A Sign of Caution

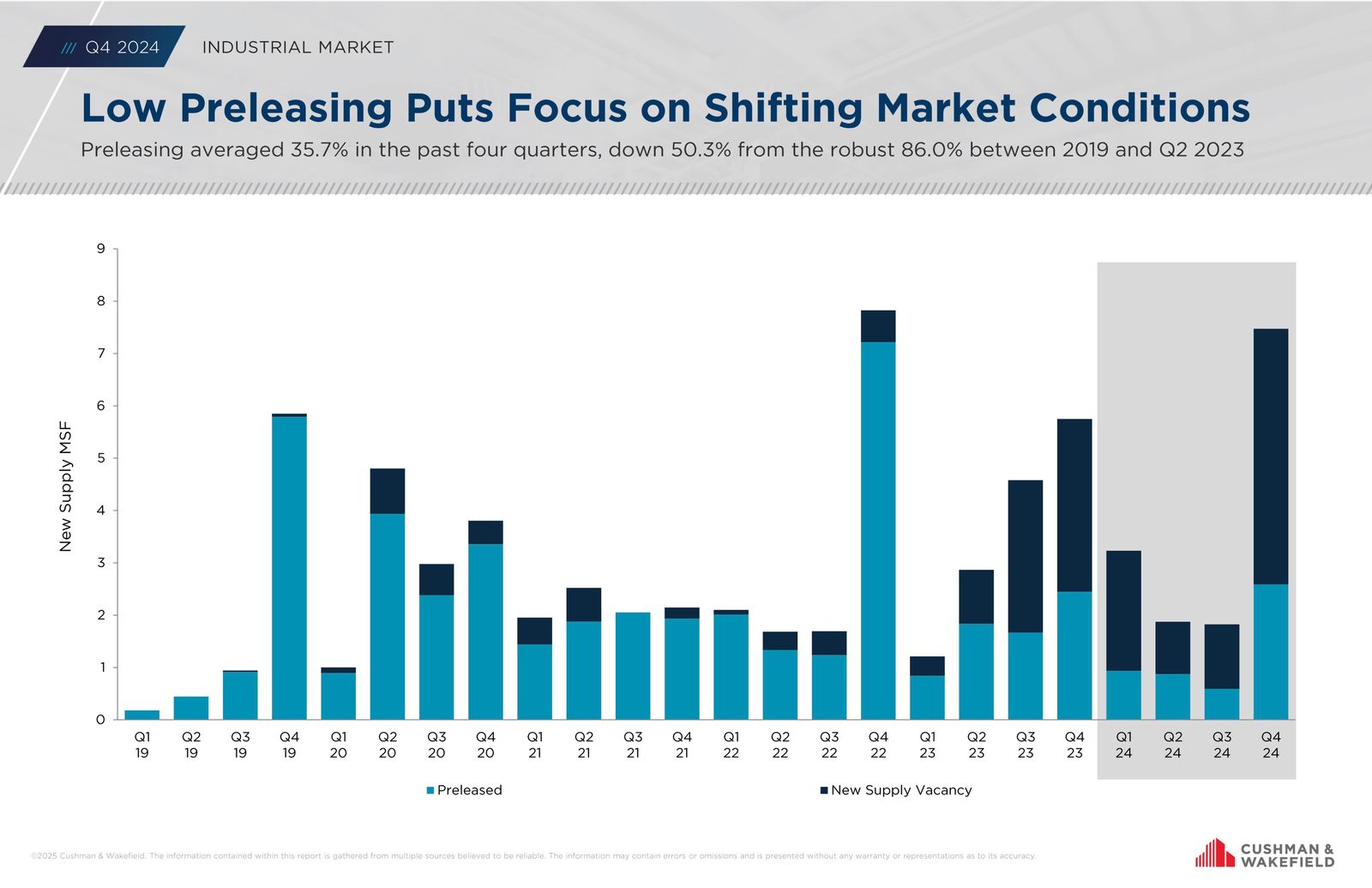

New developments are feeling the pinch too. Preleasing rates—a bellwether of market confidence—have plummeted to an average of 35.7% over the past four quarters, down from a robust 86.0% between 2019 and Q2 2023. This 50.3% drop suggests developers are struggling to secure tenants before completion, raising the specter of speculative inventory adding to vacancy pressures. It’s a stark shift from the pre-pandemic boom, when space was snapped up well in advance.

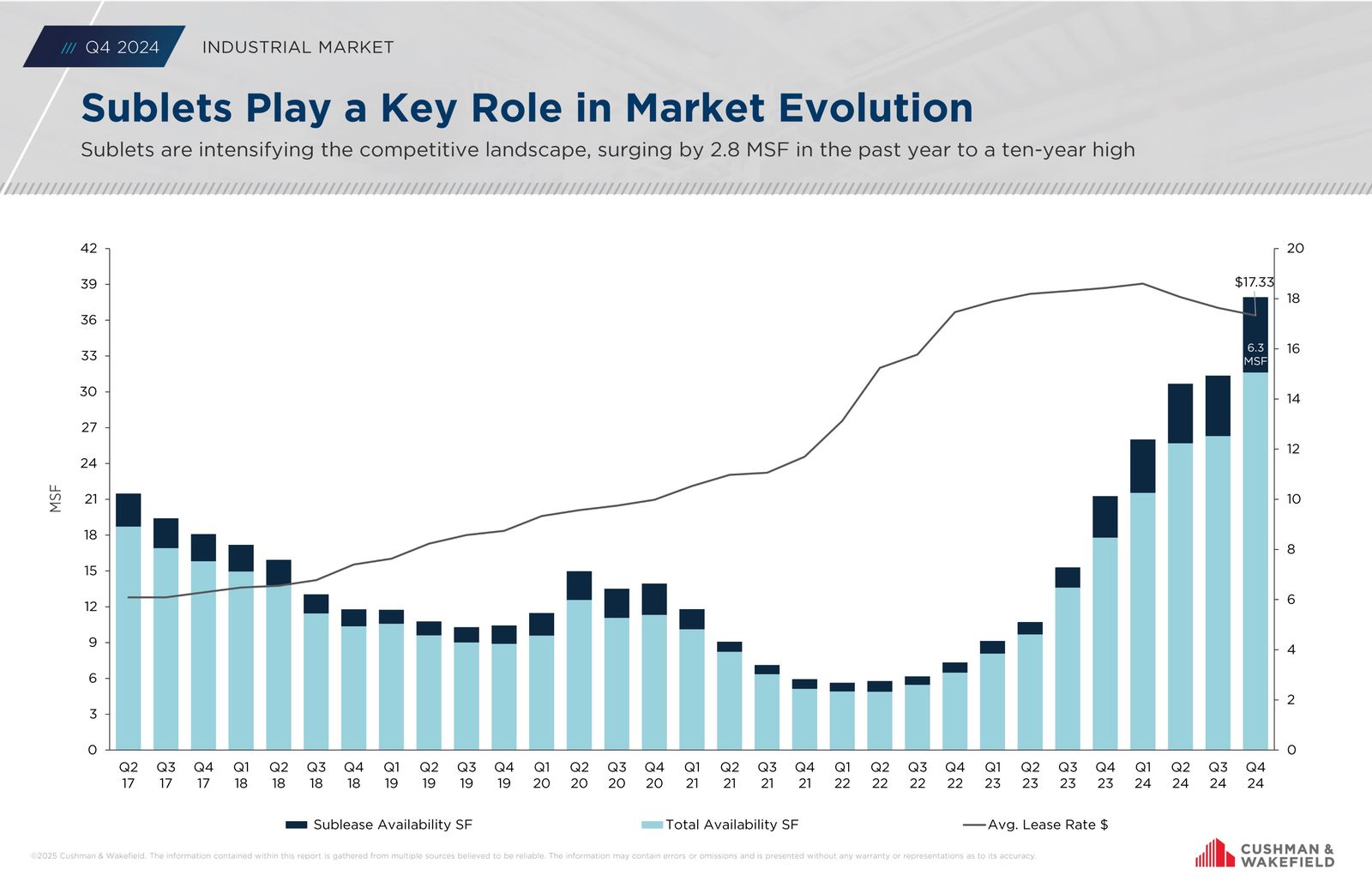

Sublets Play a Key Role in Market Evolution

A surge in sublease availability, hitting 6.3 million square feet in Q4 2024, drove total availability to a decade-high 18 million square feet. Despite this, the average lease rate rose to $17.33 per square foot. The growing sublet supply intensifies market competition, offered tenants more options and potentially curbing rental rate increases. This trend reflects evolving tenant needs and suggests a future where rental stability or moderation could dominate as supply continues to expand.

Forecast: Stability in Sight?

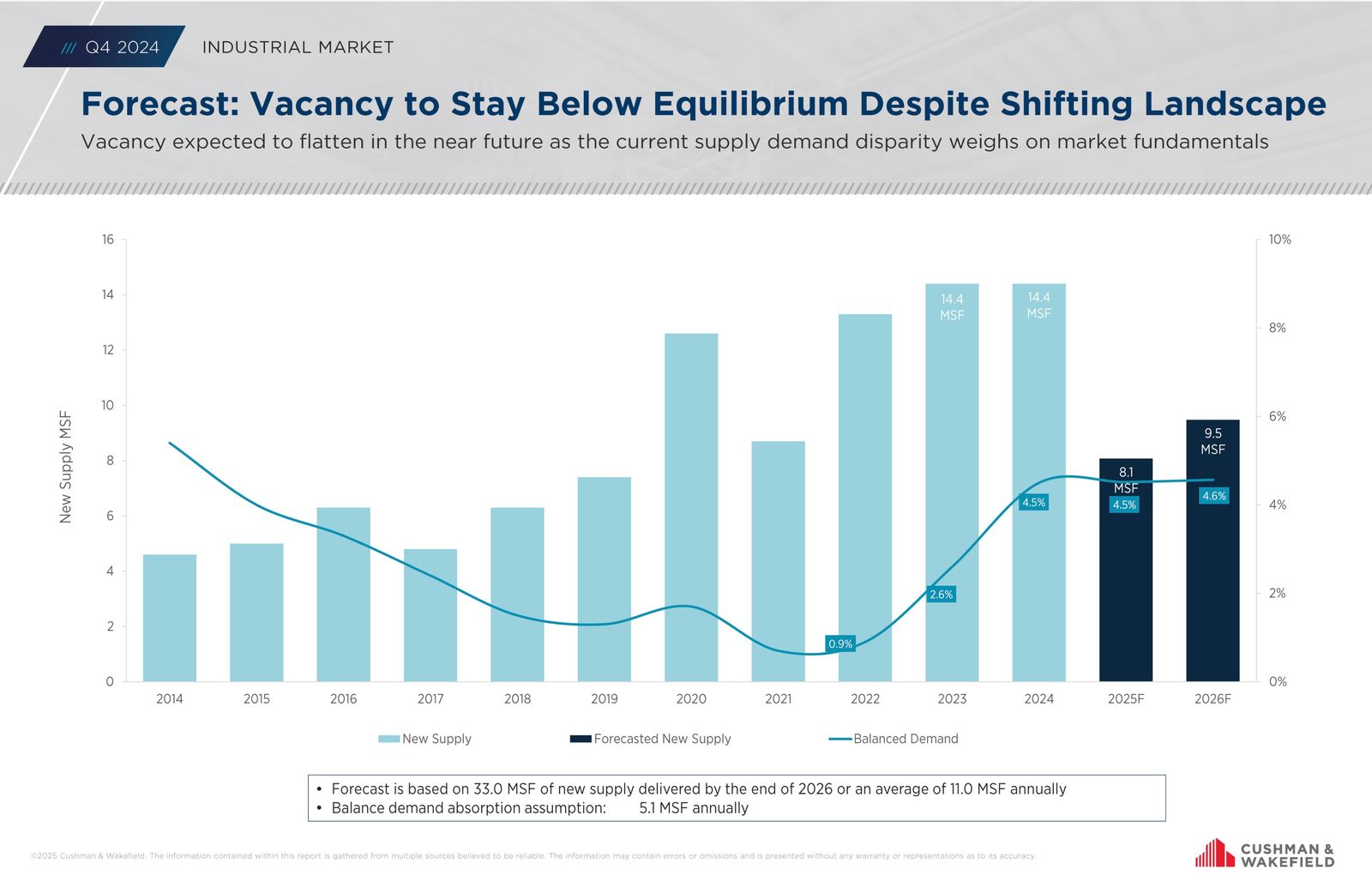

Looking ahead, the Cushman & Wakefield forecast offers cautious optimism. Vacancy rates are expected to flatten in the near future, staying below equilibrium despite the current supply-demand disparity. The projection assumes 33.0 MSF of new supply by the end of 2026 (averaging 11.0 MSF annually) and balanced demand absorption of 5.1 MSF per year. While this suggests stabilization, the gap between supply and absorption will continue to challenge market fundamentals through 2026.

Rent Trends: Modest Growth Ahead

Rental growth is forecasted to lag behind the meteoric rises of the past three years. Amid slowing demand, rents are likely to soften further in the near term before stabilizing and inching upward as the market digests new supply. The GTA’s $17.33 per square foot average may see modest gains, but don’t expect a return to 2022’s record-setting increases anytime soon.

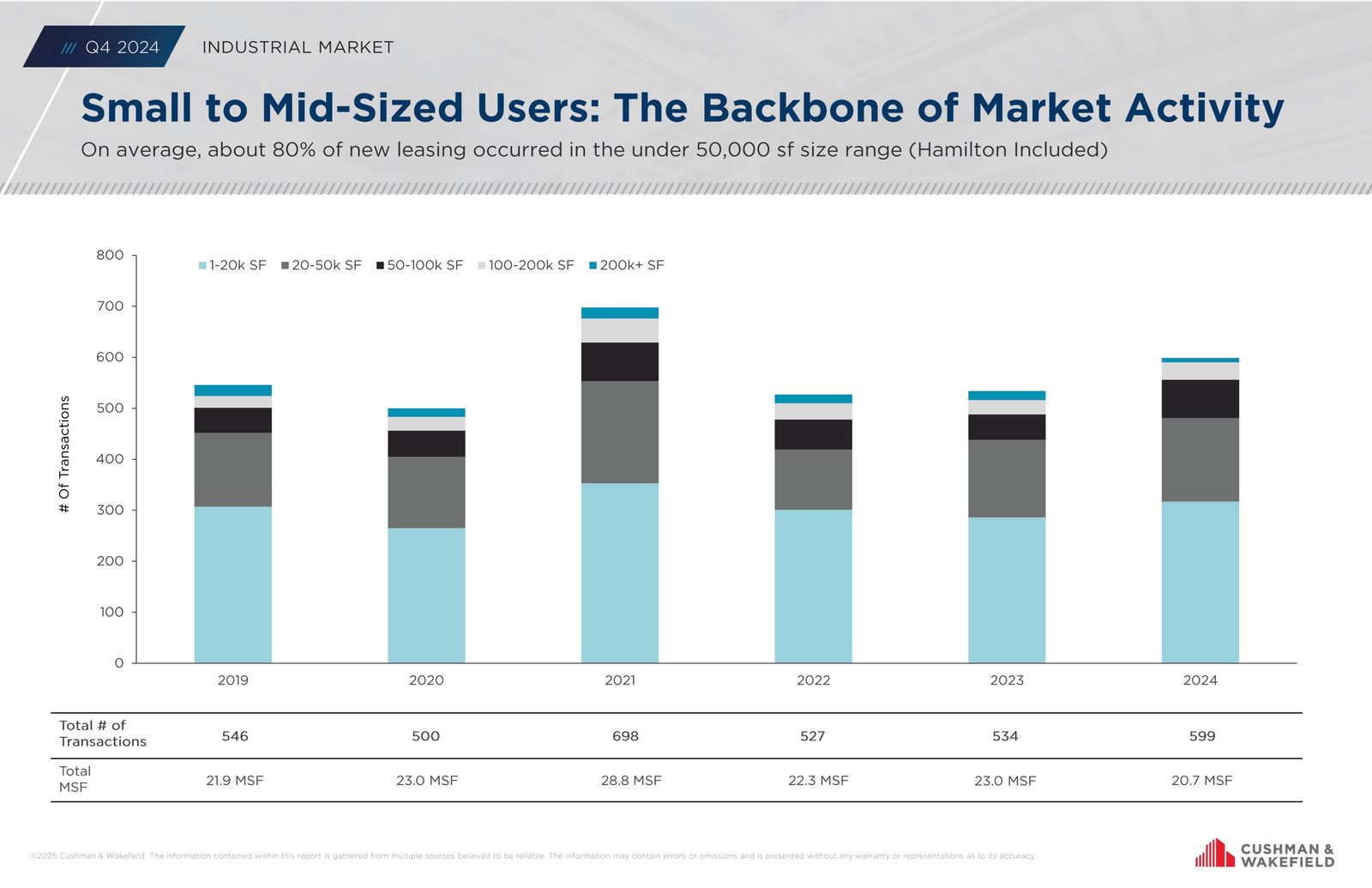

Small to Mid-Sized Users: A Steady Force Amid Shifting Rental Trends

Small and mid-sized users continue to anchor the GTA industrial market, driving roughly 80% of new leases in spaces under 50,000 square feet. From a peak of 698 transactions in 2021 to 599 deals totaling 20.7 million square feet in 2024, this segment’s consistent demand signals stability.

For landlords, this means rental rates for smaller spaces could hold firm or even edge up as tenants vie for these high-activity ranges. Investors should see this as a dependable bright spot, while tenants looking for flexibility will find plenty of options in this vibrant size category.

Strategic Takeaways

- Landlords: Flexibility—through competitive pricing or enhanced tenant incentives—will be key to filling vacant spaces.

- Tenants: Now’s the time to negotiate favorable leases, especially in oversupplied submarkets.

- Investors: Focus on properties with strong fundamentals and long-term growth potential to weather short-term turbulence.

Conclusion:

Rental rates in the GTA industrial market are softening after three quarters of decline, reflecting cautious preleasing and increased supply.

However, stabilization is on the horizon, with vacancy projected to ease below equilibrium by 2026.

Tenants can seize negotiation leverage now, while landlords and investors should prioritize flexibility and prime assets. The GTA’s high rents and strategic value ensure its long-term appeal. Reach out to discuss how these trends can inform your next steps in this evolving market.

In the meantime, for a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com