July 4th, 2025

It’s almost unthinkable that a dip to $17.00 per square foot net average rents would be considered a move ‘towards stability’ – yet that’s where we find ourselves today.

In a sense, it seemed like it was almost a foregone conclusion, except that nobody knew when it might ever occur. Would it take some sort of economic uncertainty? Or some sort of major market correction?

While things have been strained, realistically, ever since the economic lockdowns, the reality is that major corporations within the logistics, warehousing, and transportation sectors – along with related businesses in consumer products and online retail – largely drove the bus when it came to rental rates, absorption, and a spur to new development.

The smaller businesses either following behind or simply those occupying small- to mid-bay properties really felt the pinch when it came time to renew or relocate. That said, they weren’t the driving force and, through conversations on the street-level, many thought these rates were not true rates and were unsustainable. To say that a large percentage thought they could wait it out until things went back to normal would be an understatement.

However, rates are as true as the ink on lease agreements. And those agreements were very real.

Despite this, and to counter the narrative, we did see a flurry of sublease listings bubble to the surface from 2023 and into 2024 as interest rates and a fizzling out of the post-lockdown boom brought megadeals to a slow grind and final halt. Add to that the flood of new construction coming online and rates are finally beginning to course correct.

Which begs the question; what are the true rates? Well, inflation brings on ‘price stickiness’ – particularly throughout supply chains and with wages – and those input costs filter downstream into everything else. Will rates ever return to pre-pandemic single-digit levels? Likely not for Class A space, although we are seeing mid-to-high teen’s and lots of incentives to secure quality, creditworthy tenants.

So without further ado, let’s dive a bit deeper into the Greater Toronto industrial market based on the latest data from Q2 2025.

Market Snapshot

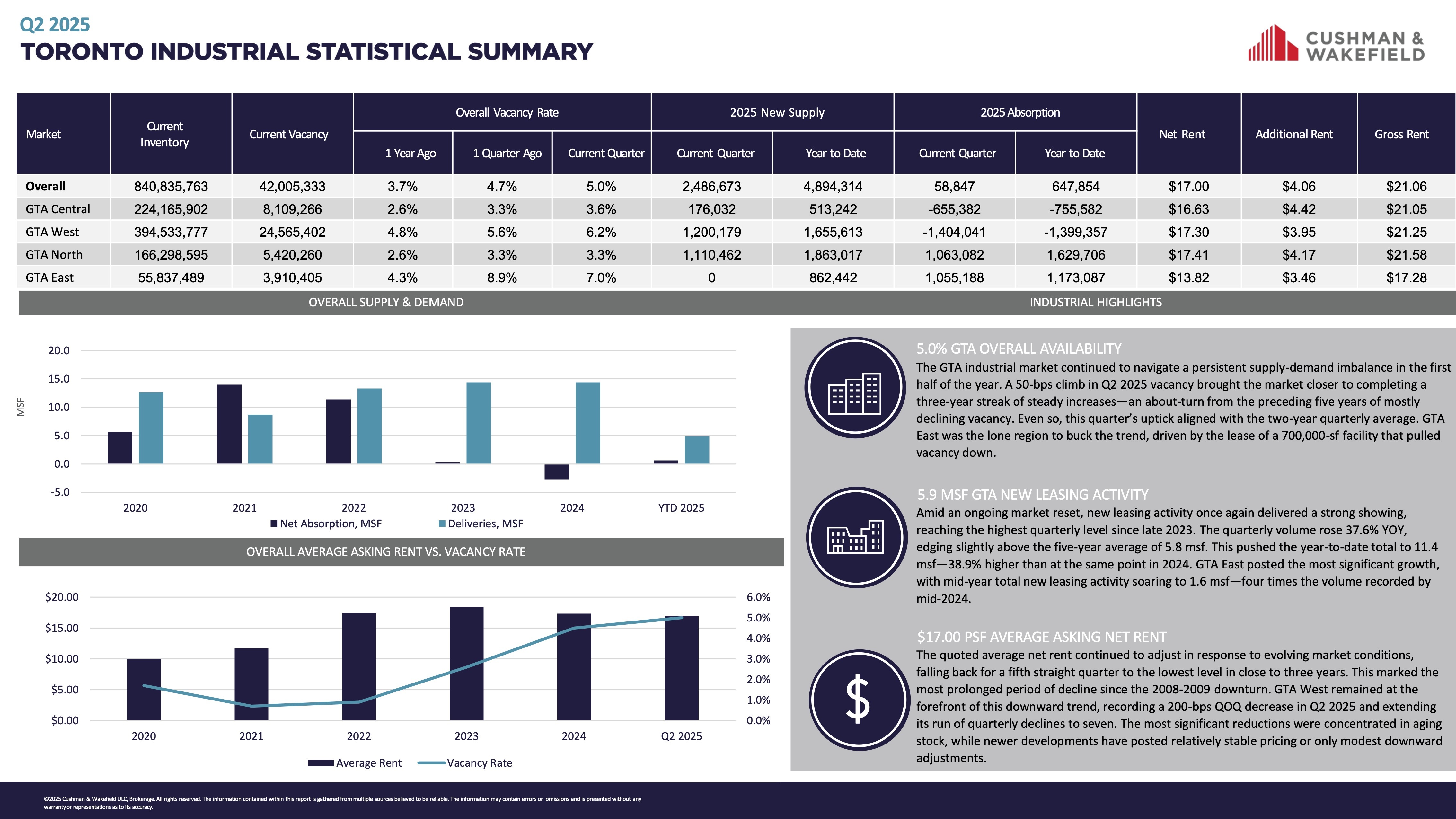

The Toronto industrial market in Q2 2025 reflects a scenario characterized by significant new supply and restrained demand. The GTA vacancy rate stabilized at 5.0%, an increase from 4.7% in the prior quarter and 3.7% a year ago, attributable to 2.49 MSF of new supply this quarter, part of a 4.90 MSF year-to-date total.

Submarket vacancy rates show diversity: the GTA East peaked at 7.0% before a 700,000 SF lease mitigated the rise, the GTA West is reported at 6.2%, the GTA Central at 5.0%, and the GTA North at 3.3%. The presence of 19.6 MSF under construction, with 65% still un-leased, indicates potential for further vacancy growth if leasing activity does not sustain its current pace. This supply pressure is a key factor shaping the market’s current state, requiring close monitoring by stakeholders to assess future impacts on availability.

Leasing and Absorption Trends

Leasing activity in the GTA reached 5.9 MSF, a 37.6% increase from 2024 and the highest since 2023, primarily driven by the 700,000 SF lease in GTA East. This figure underscores a level of tenant interest in the market despite economic challenges. In contrast, absorption remains low, with 58,847 SF recorded in Q2 and 647,854 SF year-to-date. Submarket absorption data reveals significant variation: GTA Central reported negative 655,582 SF, GTA West at negative 1,404,041 SF, GTA East at 1,055,188, and GTA North at 1,063,082 SF, indicating uneven demand across the region.

This disparity suggests that while leasing is robust for specific large transactions, overall occupancy growth is limited. Economic factors, including a 7% unemployment rate in May 2025 and ongoing trade uncertainties, may be contributing to cautious expansion decisions by occupiers. Historical trends show absorption has lagged behind deliveries since 2020, a pattern that continues to influence current market dynamics.

Rental Market Analysis

The average net rent across the GTA decreased to $17.00 PSF. Submarket rents reflect this adjustment: GTA East is at $13.82 PSF, GTA North at $17.41 PSF, GTA Central at $16.33 PSF, and GTA West at $17.30 PSF, with gross rents averaging $21.06 PSF, including $4.06 PSF in additional costs.

This decline follows a period of rent growth, and projections suggest a potential additional reduction in some areas through 2025, with stabilization anticipated by 2026. The rent decrease provides tenants with increased negotiating power, while landlords in higher-vacancy submarkets may face revenue challenges. The variation in rental rates across submarkets highlights the importance of location-specific strategies in the current market environment.

Source: Cushman & Wakefield Research.

Future Outlook

For Q3 2025, the ongoing addition of new supply could impact vacancy levels unless the 11.4 MSF year-to-date absorption trend continues. The current 58,847 SF absorption level suggests potential for growth if economic conditions improve, which could lead to more positive net absorption. The recent leasing activity, particularly the GTA East transaction, indicates demand for strategically located properties, but broader occupancy gains are necessary to balance new supply.

Rent reductions may persist, offering cost advantages to tenants, while investors might prioritize submarkets with lower vacancy rates, such as GTA North. Historical data indicates that deliveries have outpaced absorption since 2020, but the recent increase in leasing could signal a shift if sustained. The market’s trajectory will depend on economic stabilization and continued tenant engagement.

Conclusion:

The Greater Toronto industrial market in Q2 2025 records a 5.0% vacancy rate, 2.49 MSF of new supply, and 5.9 MSF in leasing, with absorption at 58,847 SF. The $17.00 psf net rent is projected to stabilize by 2026, supported by historical trends of rent adjustments following supply increases. Submarket differences, ranging from 7.0% vacancy in GTA East to 3.3% in GTA North, provide strategic options for targeting high-demand areas or negotiating favourable terms in oversupplied zones.

Stakeholders should closely monitor leasing performance and assess risks from ongoing supply additions, as sustained demand growth will be critical to absorb new capacity. The market’s resilience, evidenced by the 700,000 SF GTA East lease, suggests potential for recovery, but economic factors like unemployment and trade stability will influence outcomes.

For a confidential consultation or a complimentary opinion of value of your property please give us a call.

Until next week…

Goran Brelih and his team have been servicing Investors and Occupiers of Industrial properties in Toronto Central and Toronto North markets for the past 30 years.

Goran Brelih is an Executive Vice President for Cushman & Wakefield ULC in the Greater Toronto Area.

Over the past 30 years, he has been involved in the lease or sale of approximately 25.7 million square feet of industrial space, valued in excess of $1.6 billion dollars while averaging between 40 and 50 transactions per year and achieving the highest level of sales, from the President’s Round Table to Top Ten in GTA and the National Top Ten.

Specialties:

Industrial Real Estate Sales and Leasing, Investment Sales, Design-Build and Land Development

About Cushman & Wakefield ULC.

Cushman & Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 53,000 employees in 400 offices and 60 countries.

In 2020, the firm had revenue of $7.8 billion across core services of property, facilities and project management, leasing, capital markets, valuation and other services. To learn more, visit www.cushmanwakefield.com.

For more information on GTA Industrial Real Estate Market or to discuss how they can assist you with your real estate needs please contact Goran at 416-756-5456, email at goran.brelih@cushwake.com, or visit www.goranbrelih.com.

Connect with Me Here! – Goran Brelih’s Linkedin Profile: https://ca.linkedin.com/in/goranbrelih

Goran Brelih, SIOR

Executive Vice President, Broker

Cushman & Wakefield ULC, Brokerage.

www.cushmanwakefield.com

Office: 416-756-5456

Mobile: 416-458-4264

Mail: goran.brelih@cushwake.com

Website: www.goranbrelih.com